4 sometimes-conflicting ways I’m thinking about the economy 😬😞😎🙃

Plus a charted review of the macro crosscurrents 🔀

📈The stock market rallied to all-time highs, with the S&P 500 setting an intraday high of 6,532.65 on Friday and a closing high of 6,502.08 on Thursday. The index is now up 10.2% year-to-date. For more on the market, read: 15 charts to consider with the stock market at record highs 📊📈

-

Last year, I wrote about how there are four different ways your view of the economy can be informed: hard economic data, soft economic data, the stock market, and your personal biases.

The point is that it’s possible to have what appear to be conflicting views of the economy, even though you’re not disagreeing on the facts.

Let me demonstrate by offering my views on the current state of the economy while wearing each of these four different hats.

Hard-data hat: The economy is barely growing, and recession risk is up 😬

Hard data is anything that reflects quantifiable and observable behavior — stuff that is actually happening. These include metrics such as employment and personal spending, which help us determine whether the economy is in expansion or recession.

From the perspective of hard data, I don’t feel as great about the economy as I used to.

The hard data have cooled so much that we are arguably at an economic tipping point. Job creation has fallen to near zero, personal consumption has plateaued, industrial production is going sideways, and capex order activity is off its high.

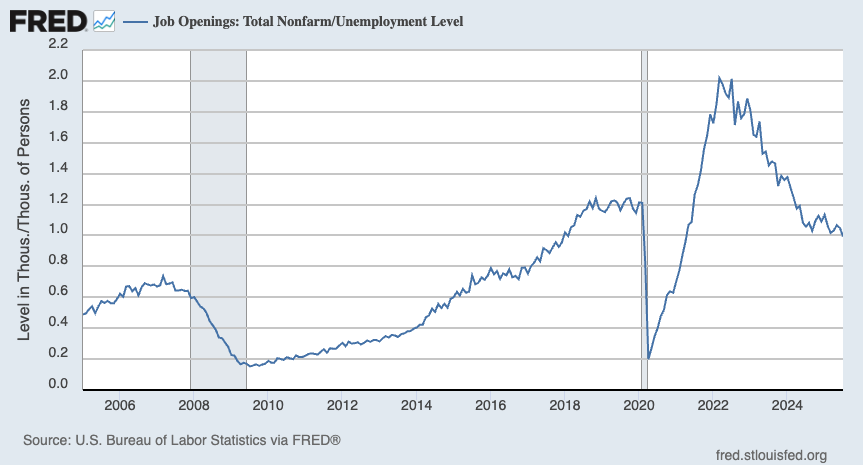

Notably, the ratio of job openings per unemployed persons fell below 1:1 in July for the first time in over four years.

While this ratio continues to suggest there are many jobs for the taking, the situation is nowhere near as robust as it was during the early stages of the current economic expansion.

Economists often discuss the relationship between job openings and unemployment with the Beveridge curve, which shows that declining job openings are correlated with rising unemployment.

“We’re operating along a segment of the Beveridge Curve where declines in excess labor demand, as proxied by falling job openings, will result in larger increases in the unemployment rate,” Renaissance Macro’s Neil Dutta wrote on Wednesday. “Not good.”

I’m not convinced that we are doomed to fall into recession. However, I think it is increasingly hard to argue that growth is destiny.

For more, read: We're at an economic tipping point ⚖️

Soft-data hat: Businesses are nervous, and people are increasingly depressed about their prospects 😞

Soft data is generated through surveys of consumers and business operators expressing their opinions, feelings, and expectations about things like job security, financial health, inflation, future business activity, and labor quality. Popular reports capturing soft data include S&P Global’s Purchasing Managers Index, the NFIB’s Small Business Optimism Index, and the University of Michigan’s Surveys of Consumers.

According to the ISM, purchasing managers have said manufacturing activity has been contracting for six straight months.

Even though the unemployment rate remains very low at 4.3%, people don’t feel great about the economy. Political polarization, social media, low-quality news organizations, and the proliferation of misinformation have all contributed to this disconnect between hard and soft data in recent years.

The Wall Street Journal recently published the results of a survey, and it was bleak. From the article:

A new Wall Street Journal-NORC poll finds that the share of people who say they have a good chance of improving their standard of living fell to 25%, a record low in surveys dating to 1987. More than three-quarters said they lack confidence that life for the next generation will be better than their own, the poll found.

Nearly 70% of people said they believe the American dream—that if you work hard, you will get ahead—no longer holds true or never did, the highest level in nearly 15 years of surveys.

The fact that the hard data has been deteriorating in recent months hasn’t helped any of this.

If there’s reason for optimism, it’s the fact that the economy has continued to grow despite all this pessimism. Imagine how much the economy might boom if sentiment made a big move upward?

Stock-market hat: Winning in this lackluster economy 😎

In the short run, the hard and soft economic data can spark volatility in the stock market. Technical factors in the markets will also move prices in the near term. Pretty much anything you imagine can affect trader decisions and investor sentiment, which in turn affects the markets over short periods of time.

But in the long run, the most important driver of stock prices is earnings.

And the outlook for earnings continues to be up.

The bullish corporate earnings story is in stark contrast to the lackluster economic growth story.

As Goldman Sachs analysts argued recently, the companies in the stock market benefit from greater international exposure, dollar depreciation, and a tilt toward large tech companies.

So while economic conditions may not be favorable for everyone, they’ve at least been favorable for the large companies that make up the stock market.

People can say whatever they want about how much stock prices have rallied in recent years, and how we may or may not be “due” for a major downturn. But I’d argue these calls lack merit if they don’t address the fact that earnings have been going up and are expected to continue going up.

For more on this, read: The stock market and the economy are diverging 📊 and What's the bottom line? 📝

My biased hat: My portfolio is hotter than my business 🙃

Some people will do poorly in a strong economy. Some will thrive in a struggling economy.

Your view on the economy will be affected by your personal circumstances.

That said, I personally have mixed emotions.

As the owner of TKer, I couldn’t be more thrilled that the stock market has been rallying to new all-time highs. After all, TKer tells the story about how the stock market usually goes up.

But the rally has ironically been a bit bittersweet. Engagement on TKer has cooled, and the pace of subscriber growth has recently leveled off. This is not surprising. In my 19 years in financial publishing, one thing I’ve learned is that reader interest is highest during market downturns and volatile periods. Meanwhile, when stock prices are trending higher — like they have been for most of the summer — fewer people are interested in better understanding what drives the market.

In other words, what’s good for your portfolio in the near-term is less than great for the financial information business. And vice versa.

So yeah, it bums me out to see that fewer people are subscribing and fewer subscribers are opening emails as the stock market sets new all-time highs.

Of course, I would never wish there to be more market volatility.

Fortunately, as a long-term investor in the stock market, I’m naturally hedged!

Zooming out 🔭

Like I said, TKer tells the story of how the stock market usually goes up. It’s a stock market newsletter.

And while I’ll continue to write about hard and soft economic data, and everything in between, it’ll always be written from the perspective of investors in the stock market.

-

More from TKer:

Review of the macro crosscurrents 🔀

There were several notable data points and macroeconomic developments since our last review: