Stocks make more sense when you look forward, not backward 🚶♀️

The once-anticipated earnings recession is becoming a thing of the past ⌛️

I can’t reiterate enough that stocks are discounting mechanisms — i.e., they price in expectations for the future.

So I’d caution against reading too much into news stories emphasizing how many companies are expected to report negative earnings growth for Q2 in the coming weeks.

Why?

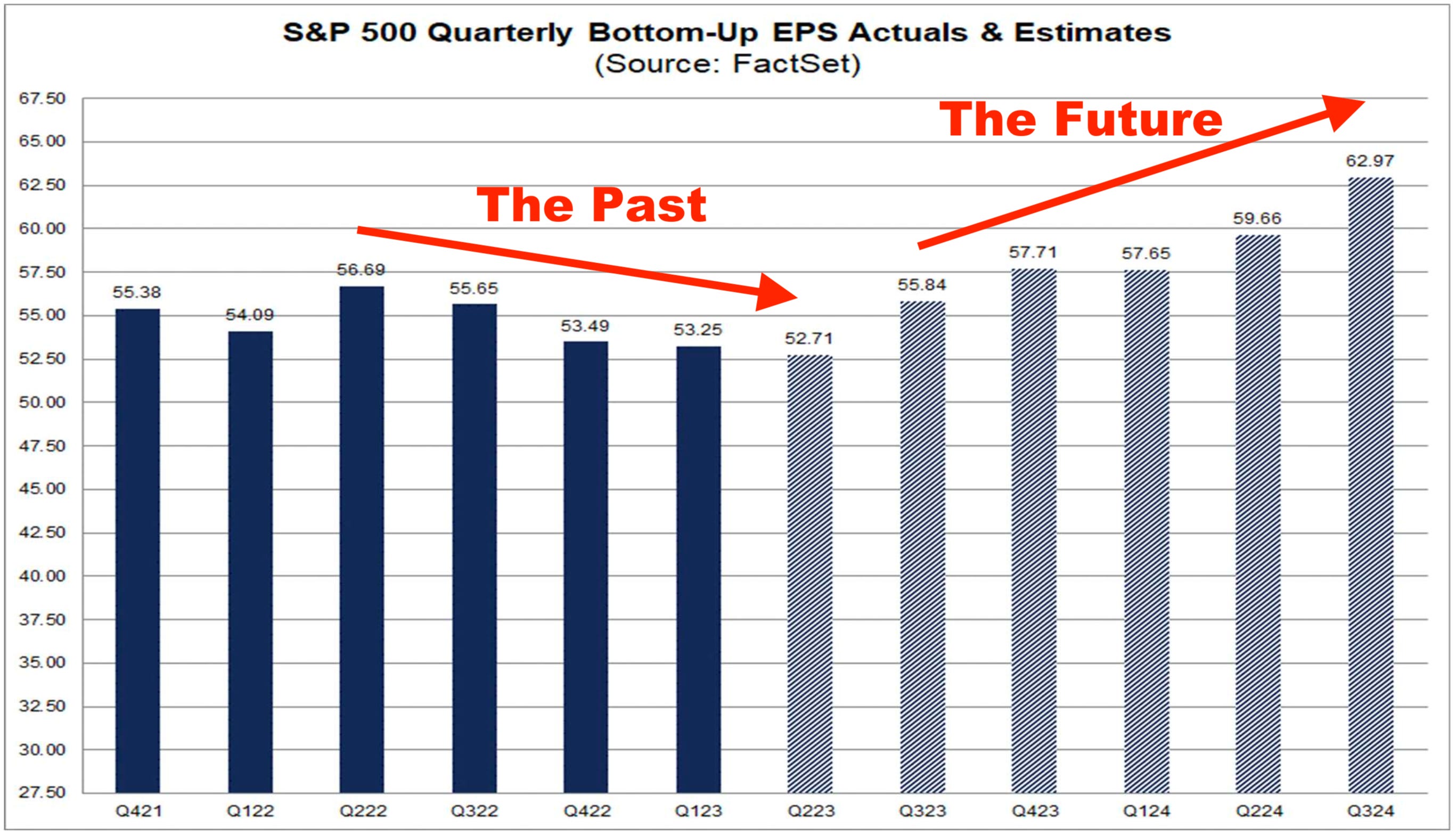

First of all, weak earnings have been widely expected for months. They were arguably the most frequently cited risk to stocks coming into 2023. According to FactSet, Q2 is likely to reflect the fifth straight quarter-over-quarter decline in S&PP 500 earnings. So it’s not a stretch to argue that the weakness in stock prices last year came in anticipation of the downturn in earnings we’re experiencing now.

Second, Q2 is expected to be the trough for earnings, and Q2 ended on June 30. It’s a thing of the past. According to FactSet, quarterly earnings growth is set to resume with Q3. So it’s also not a stretch to argue that the bull market rally we’re currently experiencing has been in anticipation of earnings growth in the quarters to come.

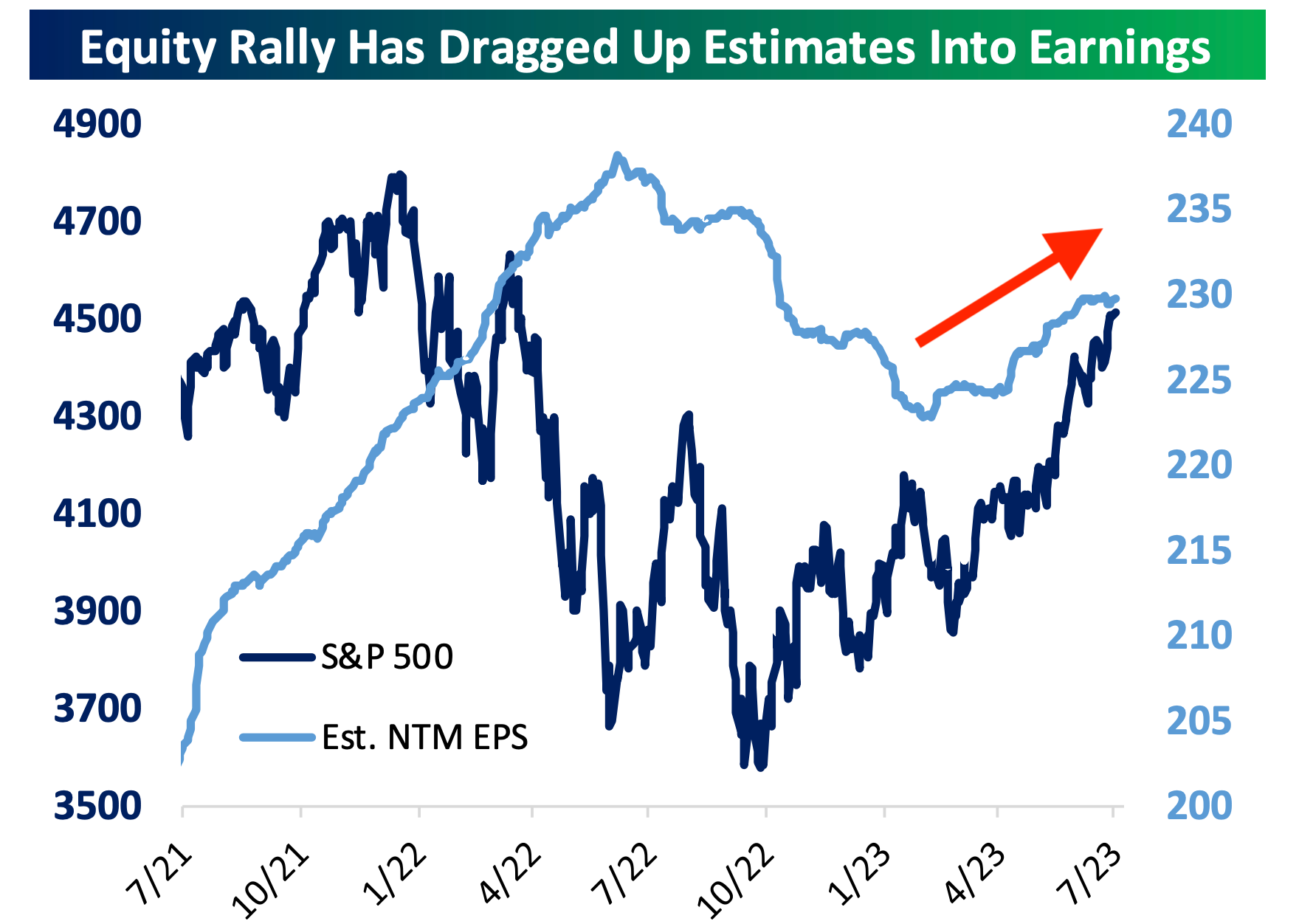

Bespoke Investment Group circulated a good chart showing the trajectory of next-12 month (i.e., forward) earnings in relation to stock prices.

“As stocks have rallied off the October lows, earnings estimates have predictably turned more bullish, with estimated next 12 month EPS bottoming at the end of February,” Bespoke analysts wrote on Monday.

So as companies report their Q2 financial results in the coming weeks, analysts and investors will be listening very carefully for anything that’ll inform those future expectations.

All eyes on profit margins 👀

Keep reading with a 7-day free trial

Subscribe to 📈 TKer by Sam Ro to keep reading this post and get 7 days of free access to the full post archives.