You don't have to look outside U.S. stocks for international exposure 🌎

Plus a charted review of the macro crosscurrents 🔀

Stocks fell last week with the S&P 500 shedding 3% to close at 4,967.23. The index is now up 4.1% year to date and up 38.9% from its October 12, 2022 closing low of 3,577.03. For more on market volatility, read: Even strong stock market years can get very stressful 😱

-

Financial advisors will often recommend clients to allocate outside of the U.S. by investing in non-U.S. stock markets. This can potentially help investors better diversify their portfolios, and in some cases, provide exposure to markets that could outperform the U.S.

But just because you only invest in U.S. stocks doesn’t mean you’re not exposed to overseas economies.

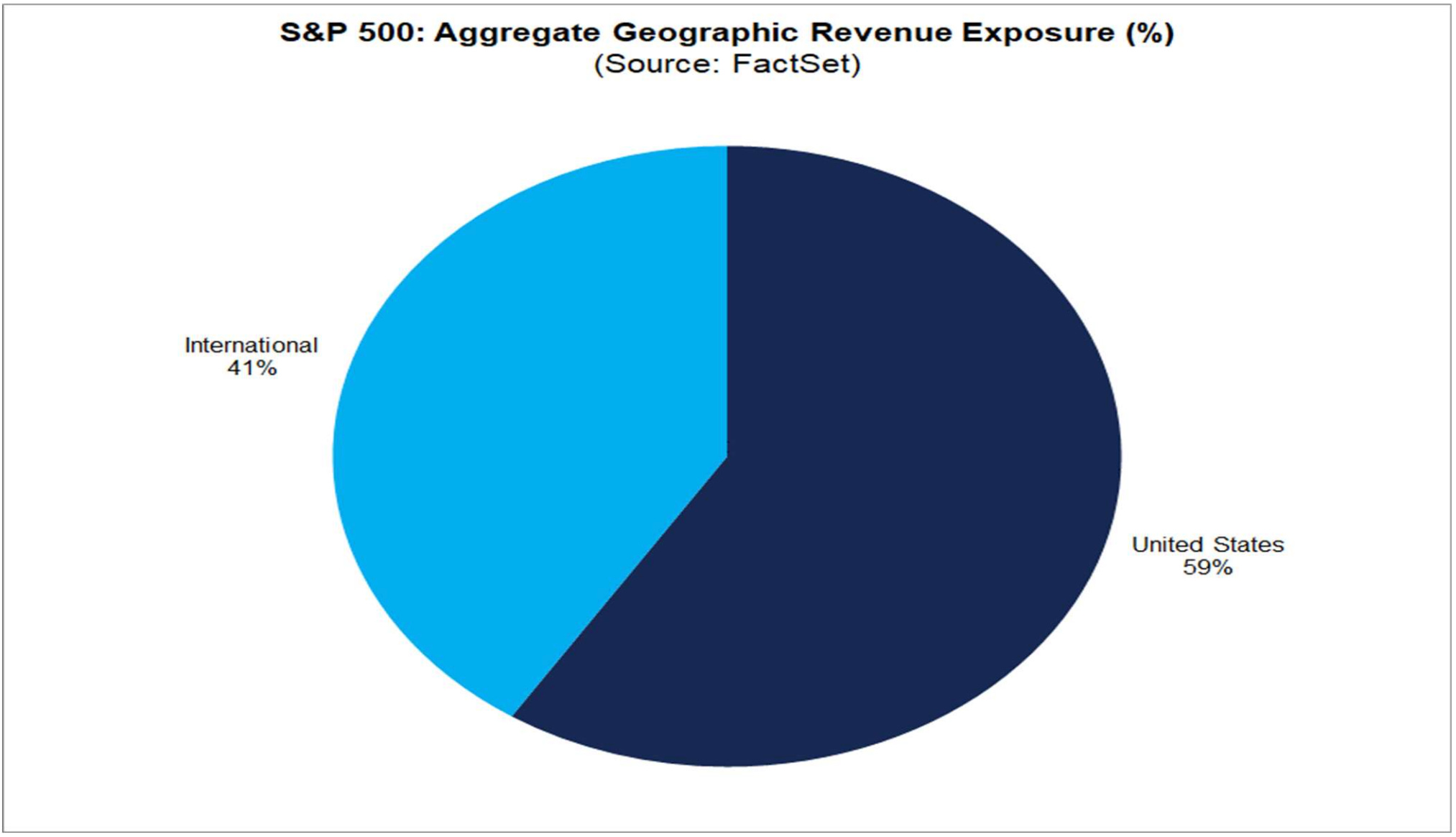

The U.S. stock market includes many multinational corporations that conduct a lot of business abroad. According to FactSet, 41% of revenue generated by S&P 500 companies comes from international markets.

Sure, we’re only talking about the S&P 500 here. But the combined market cap of these companies represents a little over 80% of the market cap of all publicly traded U.S. stocks.

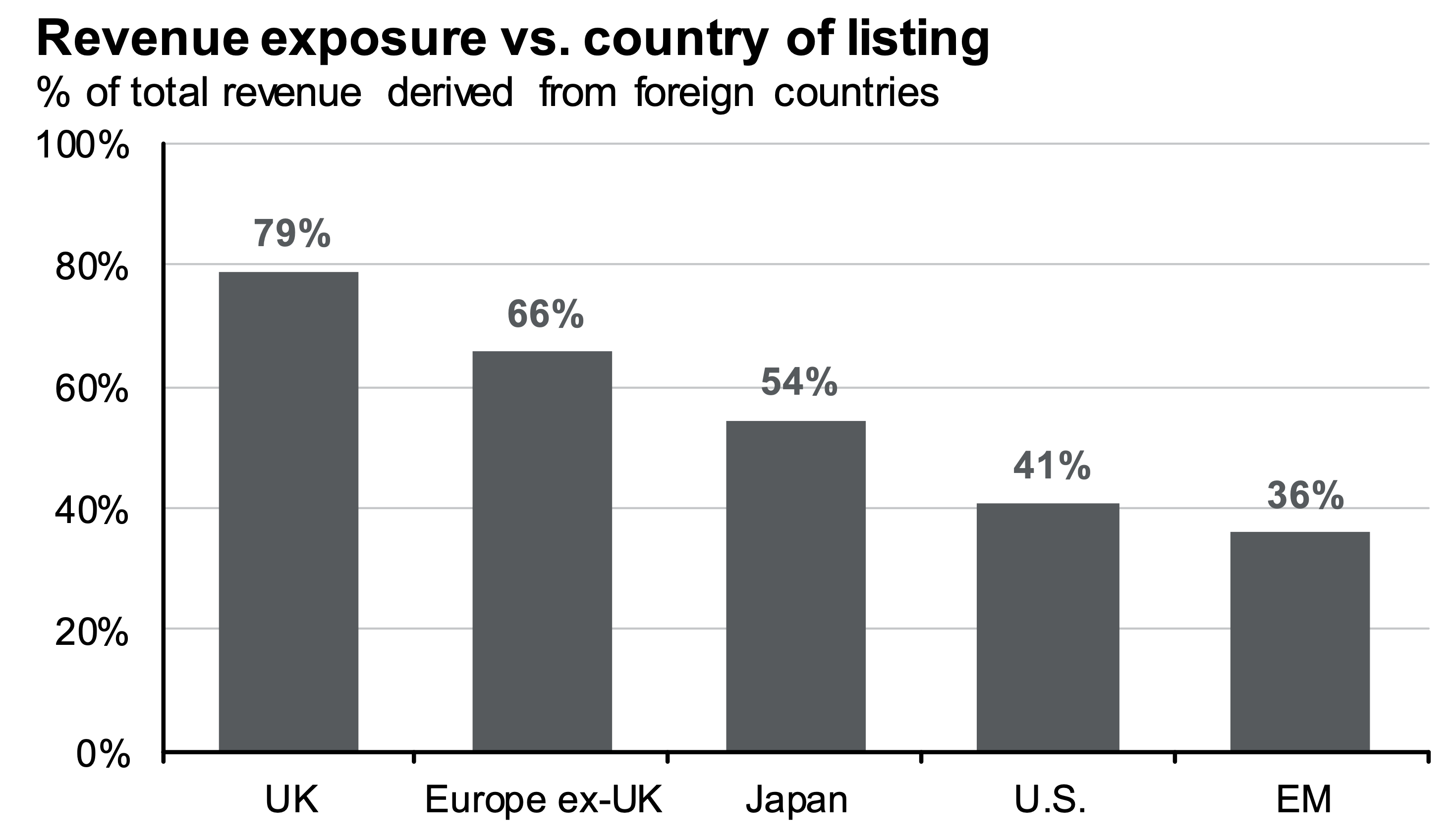

It’s worth noting that’s it’s not just U.S. companies that do business outside of their home countries. As this chart from JPMorgan shows, companies listed abroad similarly do lots of business outside of their own regions.

Of course, many large non-U.S. companies sell a lots of goods and services to U.S. customers, which means investing in non-U.S. stocks can be a way to indirectly get some exposure to the U.S. economy.

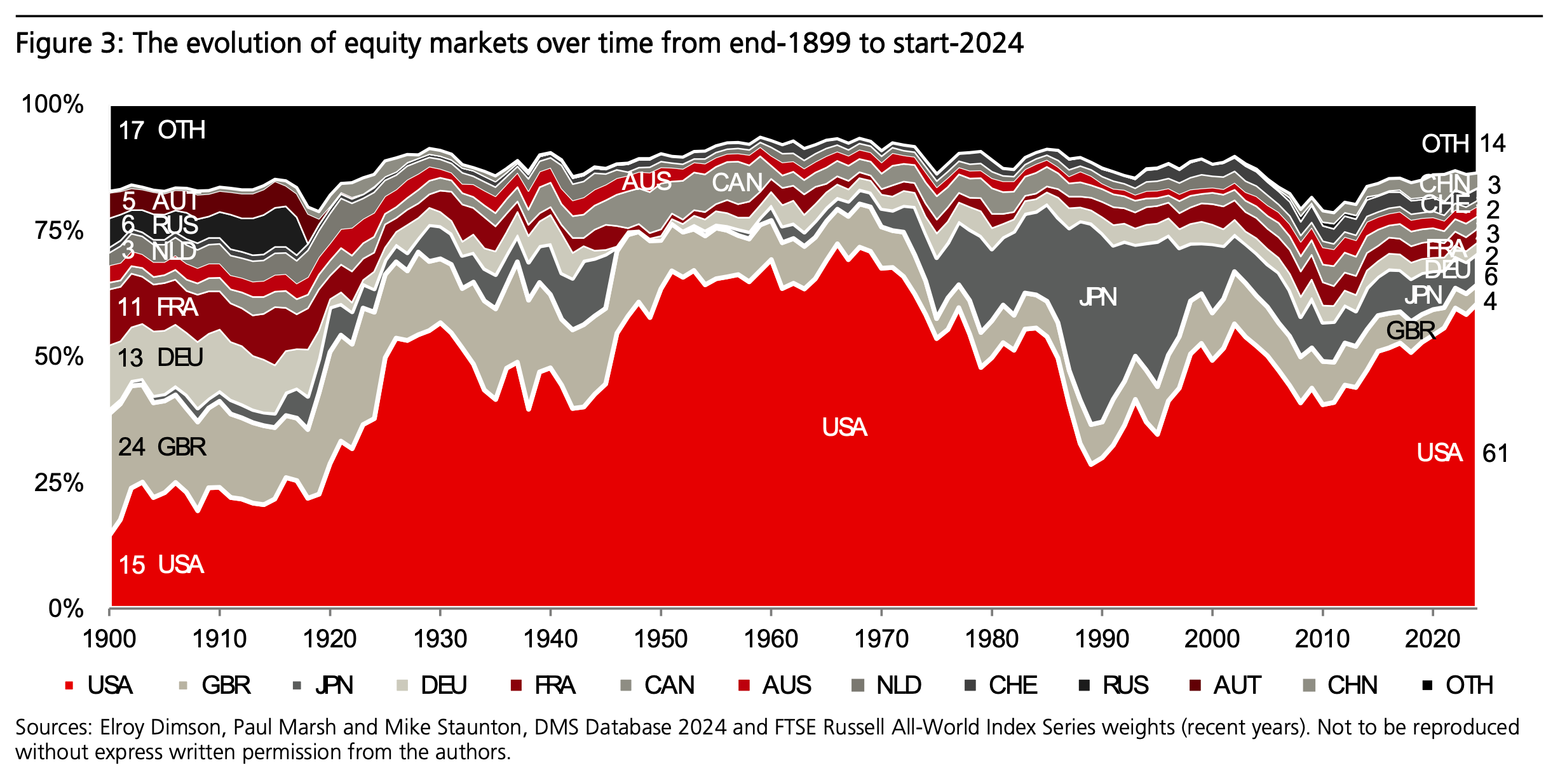

None of this is to say there aren’t great opportunities for investors in non-U.S. stock markets from time to time. The chart below from UBS is a good illustration of this. It shows how the share of the world stock market’s value shifts across regions over time. During the periods when the U.S. (in red) was expanding, it was growing as a share of the world market, which implies that its market was outperforming the rest of the world. When the U.S. was contracting, it was underperforming the rest of the world, which means investors could’ve benefited from having greater exposure to non-U.S. markets during these periods.

There’s much more to be said about investing in companies based outside of the U.S. But for the purposes of this discussion, the bottom line is that you’re already getting lots of exposure to international companies by investing in the U.S.-based stocks of the S&P 500.

The U.S. stock market is exceptional 🇺🇸

It can’t be reiterated enough that the U.S. stock market is absolutely massive. According to UBS, the U.S. market represents about 60% of the value of the entire world stock market.

There’s clearly something special going on right now in the U.S. that helps explain why its stock market has performed so well on the global stage. Maybe it’s the culture of innovation. Maybe it’s the business-friendly regulation. Maybe it’s the relatively strong corporate governance practices. Maybe it’s how shareholders incentivize company executives and employees.

Whatever it is, it’s helping to drive earnings higher. As a result, investing in the U.S. stock market has been a winning trade for a long time, and there’s little reason to believe it won’t continue to be in the years to come.

Zooming out 🔭

Whether it’s loading up on certain stocks, shifting weights towards certain sectors, or increasing exposures to certain overseas stock markets, there seems to be no shortage of ways to tweak your portfolio in ways that may or may not increase your future returns.

But just because you have most of your equity allocation sitting in the U.S. stocks of the S&P 500 doesn’t mean you aren’t already broadly diversified across businesses and industries across the world.

-

Related from TKer:

4 key observations about the U.S. stock market to remember 📊

A very long-term chart of U.S. stock prices usually going up 📈

Watch! 📺

I caught up with J.C.Parets and Spencer Israel on StockMarketTV! We discussed evolving market narratives, the outlook for financial media, and more! Check it out on YouTube here! (I come in at the 28 minute mark.)