There's more upside than downside for long-term investors 📈

Plus a review of the macro crosscurrents 🔀

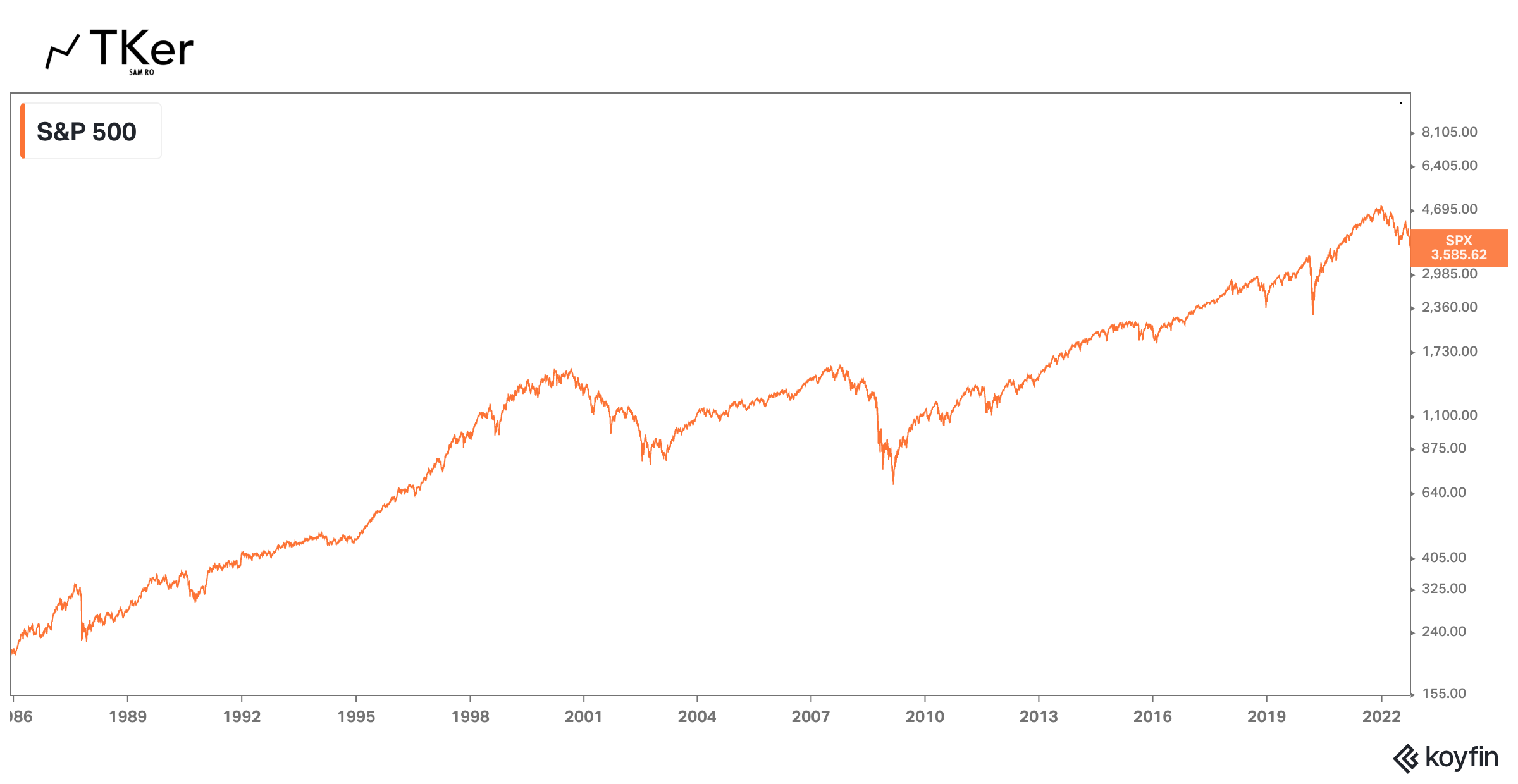

Last week, stocks tumbled to their lowest level since November 2020. The S&P 500 fell 2.9% to close the week at 3,585.62. The index is now down 25.2% from its January 3 closing high of 4,796.56.

There were some unnerving developments in the world in recent days.

The U.K. government unexpectedly announced tax cuts that sent the British pound tumbling and …