When the Fed-sponsored market beatings will end 📈

Eventually, the Fed will get out of the market's way. But it could be months. ⏳

Investors are coping with a dreadful bear market in stocks.

At some point in the future, we’ll learn a new bull market in stocks has begun.

But before we can get there, the Federal Reserve will have to take its foot off the neck of financial markets.

The stock market’s conundrum

With inflation anything but under control, the Fed has been actively and explicitly doing what it can to rein in the financial markets in its effort to cool demand in the economy, with the ultimate aim of bringing down inflation.1

The Fed got extra hawkish in June after an unexpectedly hot consumer price index (CPI) report debunked the idea that inflation had peaked two months earlier.

At the central bank’s June policy meeting, Fed Chair Jerome Powell all but confirmed that the bank is hoping for a bear market, saying, “Over the course of this year, financial markets have responded and have generally shown that they understand the path we're laying out.”

Vickie Chang, global markets strategist at Goldman Sachs, explained this dynamic in a June 14 research note (emphasis added):

“The recent market correction has been a Fed-driven one, as equities have steadily priced in more tightening this year while simultaneously worrying that such front-loaded tightening will ultimately lead to a policy reversal. Our US economists also do not see major financial imbalances of the sort that led to the retrenchment episodes of the 2000s. So, for equities to recover in a sustained way, history suggests that this kind of monetary tightening-induced contraction is most likely to end when the Fed shifts policy direction. While a shift towards Fed easing is unlikely without an outright move into recession, as in late 2018, a clear signal that tightening risks are receding may be sufficient.”

So we have financial markets being held hostage by the Fed until it sees “clear and convincing” evidence inflation is cooling.

Until we get that evidence, the central bank does not want to see things like falling interest rates and higher stock prices. They would reflect easing financial conditions, which would stimulate demand in the economy, which in turn could keep inflation high.

And now, we await that signal that the Fed will ease up.

When the stock market inflected during the four decades ago

The inflation rate is sitting at its highest level since 1981.

Then-Fed Chair Paul Volcker famously employed extremely hawkish monetary policy in his battle to bring down inflation. His efforts rocked the markets and sent the economy into recession.

There are many things different about the world today when compared to four decades ago. But it’s not totally ridiculous to say that what Powell faces today is similar to what Volcker faced back then. And so, maybe there are insights we can draw from that historical experience.

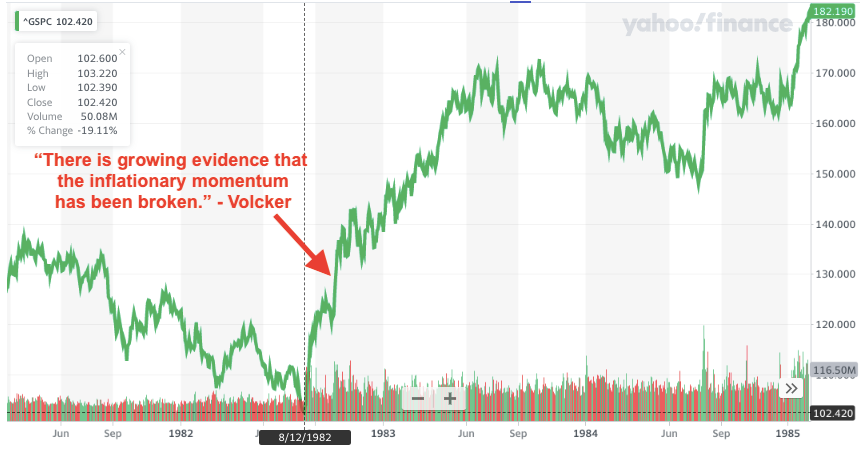

Tom Lee, head of research at Fundstrat Global Advisors, reviewed this period and found the stock market bottomed before Volcker signaled inflation appeared to be under control.

The S&P 500 hit a trough on August 12, 1982, two months before Volcker said, “There is growing evidence that the inflationary momentum has been broken.“

The story made page one of The New York Times.

From the article (H/T Fundstrat):

Paul A. Volcker, chairman of the Federal Reserve Board, said today that he considered inflation under control and that he now wanted to help try to pull the economy out of the recession.

Anticipation of such a shift, signaled by recent declines in interest rates, has ignited two sharp surges in buying on the stock markets, in August and again this week.

[…]Based on Mr. Volcker's remarks, action by the Federal Reserve to further reduce inflation, such as raising key interest rates, appears improbable any time soon. ''There is growing evidence that the inflationary momentum has been broken,'' Mr. Volcker said. ''Indeed, with appropriate policies, the prospects appear good for continuing moderation of inflation in the months ahead.''

By the time the article was published, the market was off its low. But there were still plenty of gains to be had.

Remember: The stock market is a discounting mechanism, meaning that it trades on future expectations. It falls before earnings growth turns lower, it rallies before the economy emerges from recessions, and — as Lee observed — it bottoms before an official Fed announcement of a dovish policy shift.

And so we shouldn’t be surprised to learn in hindsight that the stock market began its sustained rally before we got confirmation that inflation was indisputably trending lower and a signal from the Fed that it may soon be time to ease up on monetary policy.

When could we get the signal?

Keep reading with a 7-day free trial

Subscribe to 📈 TKer by Sam Ro to keep reading this post and get 7 days of free access to the full post archives.