There's more to the story than 'high interest rates are bad for stocks' 🤨

Theory and practice are two very different things 🤔

[WARNING: We’re gonna be addressing a complicated topic that’s usually reserved for dense textbooks. But it’s all relevant for investors who want a better understanding of what moves markets. So this is my attempt at offering some high-level, plain-English perspective.]

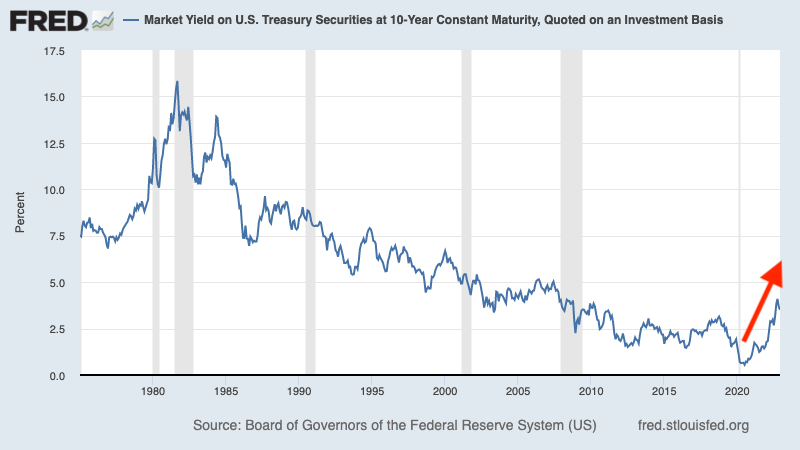

Long-term interest rates, while down from recent highs, have trended higher over the past two years from multi-decade lows.

Rising interest rates are a headwind for stock prices. It’s a phenomenon supported by finance theory. (I’ve addressed this in passing here and here.)

Today, I’m going to expand on why that’s the case. And then I’ll discuss why it might not be a big deal for long-term investors.

A bunch of ways higher interest rates are bad 👎

For the purposes of this discussion, we’re considering the perspective of businesses’ underlying stocks.

Lower sales: All other things being equal, when borrowing costs are higher, customers buy less stuff. It’s more expensive for customers to finance new stuff, and higher interest on existing debts means less money left over to buy new stuff.

Higher interest expense: All other things being equal, higher interest rates mean your borrowing costs are up. Interest on floating rate debt goes up. And any fixed rate debt will have to be refinanced at a higher interest rate. All of this means less money hits your business’ bottom line.

Smaller discounted cash flows: The projected future cash flows of your business are now being discounted to the present using a higher interest rate, which means the present value of your future cash flows are now smaller. For instance, a million dollars of profit you expect to earn in 2030 is worth less today if the discount rate is 6% instead of 3%. All other things being equal, the theoretical value of your business is now smaller.1

Speaking more broadly, higher financing costs (i.e., a higher cost of capital) justifies lower valuations in the stock market.

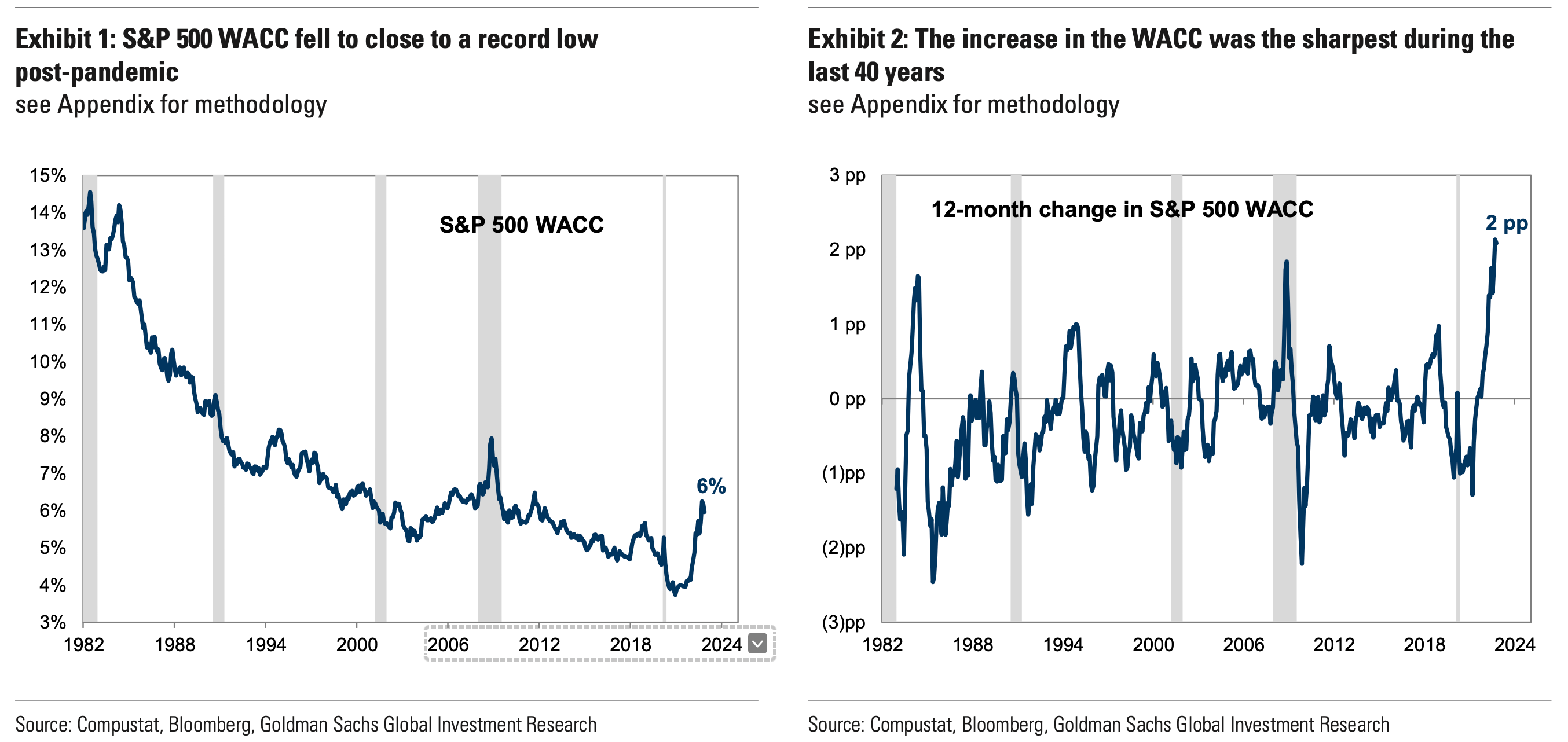

It’s big enough of an issue that Goldman Sachs analysts led with it in their 29-page research report outlining their 2023 outlook for the stock market. From the report:2

The cost of money is no longer next to nothing. The weighted average cost of capital (WACC) for US firms late last year was close to the lowest level in history. Today, following a determined effort by the Federal Reserve to curb elevated inflation, financial conditions have tightened dramatically. The WACC has spiked by 200 bp to 6%, the highest level in a decade and the largest 12-month rise in 40 years. It will remain near the current level in 2023. Sharply reduced valuation for public and private firms is one painful consequence.

So if you're thinking about stock prices from the perspective of a discounted cash flow model, which is sound in theory, then higher interest rates are a pretty big problem.3

That is, all other things being equal.