11 ways cynics argue any news is bad news 👎

Plus a charted review of the macro crosscurrents 🔀

Stocks closed higher last week with the S&P 500 gaining 2.3%. The index is now up 15.9% year to date, up 24.4% from its October 12 closing low of 3,577.03, and down 7.2% from its January 3, 2022 record closing high of 4,796.56.

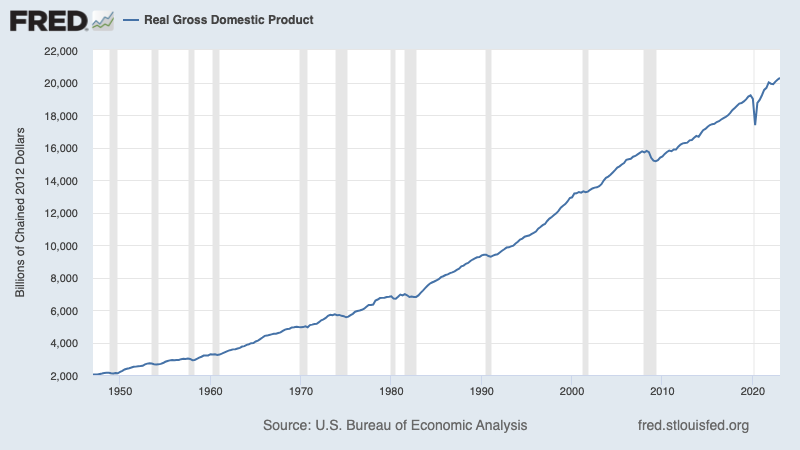

Economic data has been trending favorably. Last week, we got bullish updates on durable goods orders, business investment activity, new home sales, home prices, consumer confidence, and initial jobless claims. GDP is a bit more backward looking, but on Thursday we learned it grew in Q1 at a much faster pace than previously estimated. See more in TKer’s review of macro crosscurrents below.

The fresh data adds to reasons why many bearish economists have been dialing back their calls for a recession. It also confirms all the reasons for optimism coming into 2023.

But if you follow financial TV news, business newspapers, or social media, you’ll see there is no shortage of skeptics anchored in stale recession calls who’ll go to great lengths to spin good data into something less rosy.

“Wall Street has had recession on the brain since at least mid-2022,” Neil Dutta, head of economics at Renaissance Macro Research, wrote on Monday. “Analysts have a tendency of falling in love with their forecast, and it is clear some are having trouble letting go even as evidence piles up to the contrary.“

Earlier this year, I started to notice that regardless of whether a market or economic metric went up or down, there were bears coming out to explain why the development was bad regardless of the direction.

My friend Michael Antonelli, veteran market strategist at Baird Private Wealth Management, gave me a nudge and let me know this has always been the case for the bears.

“If you work in this industry long enough you’ll find out that things are bad both ways,” he tells me. “Why? Because pessimism sells.”

Michael and I have been flagging some of these “bad both ways” narratives as they arise. Here’s a summary:

👎 Oil prices: When they’re rising, it’s bad because hit hurts consumer spending and it drives inflation higher. When they’re falling, it’s bad because they must be a sign of weakening demand, which means we could soon learn the economy went into recession. (Michael)

👎 Home prices: When they’re up, it’s bad because it means fewer people can afford to buy. When they’re down, it’s bad because existing home owners are seeing their net worth shrink and some could go underwater on their mortgage. (Sam)

👎 Walmart sales: When Walmart sales disappoint, it’s a bad sign since they are an economic bellwether as the world’s largest retailer. When Walmart sales boom, it’s a bad sign for the economy because it must reflect financially stretched consumers trading down from higher priced retail options. (Sam)

👎 Lending activity. When businesses and consumers borrow more, it’s bad because the leverage they’re taking on puts them at greater risk of financial distress. When they borrow less, it’s bad because they aren’t taking advantage of leverage to amplify their returns on capital. (Sam)

👎 Short-term interest rates: When they’re rising, it’s a bad because it reflects worries about higher inflation and tighter Fed monetary policy. When they’re falling, it’s bad because it suggests slowing economic activity. (Michael)

👎 Long-term rates: When they’re rising, it’s bad because borrowing costs are increasing and the discount rate used to value assets is higher. When they’re falling, it’s bad because — similar to falling short-term rates — it suggests slowing economic activity. (Sam)

👎 Market volatility. High volatility is bad because it reflects elevated uncertainty, and “markets hate uncertainty.” Low volatility is bad because it must reflect complacency in financial markets, leaving them vulnerable to a major selloff when bad news breaks. (Michael, Sam)

👎 Consumer spending: When it’s falling, it’s bad because consumer spending is the dominant driver of GDP so it must mean recession risks are rising. When it’s rising, it’s bad because it’s inflationary and may lead to unfriendly actions from policymakers. (Michael)

👎 Debt ceiling: Not raising it is bad because we’d get catastrophe in financial markets if it’s breached. Raising it is bad because it gives the green light for the Treasury to sell a ton of bonds, which could drain liquidity and in other asset classes. (Sam)

👎 Mega cap growth stocks. The market must be sick when the biggest stocks are lagging the major market indexes. But it’s just as bad when the biggest stocks lead gains because they mask weakness in underperforming names. (Michael)

👎 Student loan payments. When the payments are paused, it presents moral hazard for borrowers while also enabling inflationary spending activity. But when payments resume, it’s bad because now consumer spending will dry up causing recession. (Michael)

For more, read: What the restart of student loan payments could mean for the economy 🎓

For a while, there was actually a period when “good news was bad news” in that favorable short-term moves in the economy were arguably exacerbating inflation and forcing the Federal Reserve to be increasingly hawkish with monetary policy.

But in recent months, inflation has been cooling and the Fed has been dialing back its hawkish tone. Indeed, we seem to be realizing the bullish goldilocks soft landing scenario where good news about the economy is good news as it is not fanning the flames of inflation.

For more on this outcome read: The bullish 'goldilocks' soft landing scenario that everyone wants 😀

Don’t the bulls also spin data their way?

Of course, the bulls can easily say the opposite of most of the things said above.

TKer and it’s founder have similarly been accused of tilting toward glass-half-full perspectives.

But there’s one big difference between the bulls and the bears: The bulls are usually right.

Just look at long-term charts of GDP, corporate earnings, or the stock market. All of them go up and to the right.

And I’d argue this isn’t a coincidence. Rather, it’s supported by the interests and motivations of everyone participating in the markets and the economy. As I wrote in “10 Truths About the Stock Market”:

There are way more people who want things to be better, not worse. And that demand incentivizes entrepreneurs and businesses to develop better goods and services. And the winners in this process get bigger as revenue grows. Some even get big enough to get listed in the stock market. As revenue grows, so do earnings. And earnings drive stock prices.

Over very short-term periods of time, things might be just as likely to go wrong as they are likely to go right. But over time, things tend to go right.

When you’re bullish, you’re essentially in line with what’s happened in the past and what the majority hope and expect for the future.

When you’re bearish, it’s certainly possible that you’re proven right over short periods of time. History is riddled with instances where the bears nailed their calls.

However, the longer you stay bearish, the more you’ll find yourself on the wrong side of reality. And you’ll strain as you struggle to explain why good news is bad.

It’s certainly possible that tomorrow, things will start to go down in the markets and the economy. But for now, the data is very clearly saying things are going up.

-

Related from TKer:

Keep reading with a 7-day free trial

Subscribe to 📈 TKer by Sam Ro to keep reading this post and get 7 days of free access to the full post archives.