Expectations for S&P 500 earnings are slipping 📉

The key long-term driver of stock prices 😞

Here’s how I ended the July 30 issue of TKer, which addressed cuts to earnings estimates:

With inflation problems persisting, we can expect the Federal Reserve to continue tightening financial conditions in its effort to slow the economy, which could lead to further cuts to expected earnings. This represents a big headwind for the markets as earnings are the most important long-term driver of stock prices.

Since then, the economy has continued to cool, the Fed has renewed its commitment to tighten financial conditions, and earnings expectations have continued to decline.

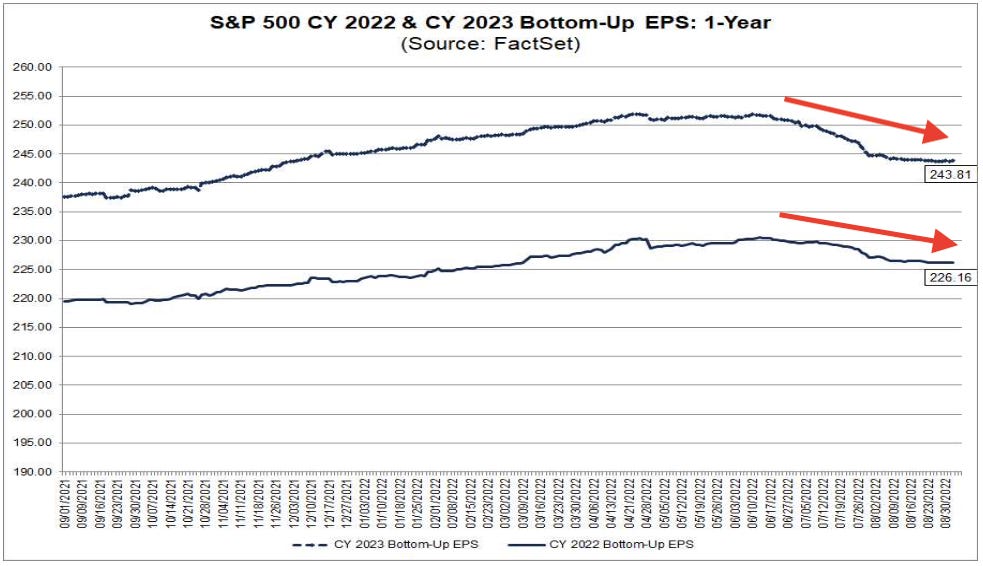

Estimates for S&P 500 earnings in 2022 stood at $226.15 per share as of August 31, according to FactSet. This is down 1.5% from the $229.60 per share estimate as of June 30.

For 2023, analysts now expect EPS of $243.68, down 2.8% from the June estimate of $250.61.

While Q2 earnings season actually proved better than expected, intensifying worries about an economic downturn in the coming quarters have corporate executives sounding caution and analysts cutting near-term estimates by more than average. From FactSet:

“The Q3 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q3 for all the companies in the index) decreased by 5.4% (to $56.21 from $59.44) from June 30 to August 31.

In a typical quarter, analysts usually reduce earnings estimates during the first two months of a quarter. During the past five years (20 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 1.9%. During the past ten years, (40 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 2.7%. During the past fifteen years, (60 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 3.5%. During the past 20 years (80 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 2.9%.”

All of this is very important: As Tker readers know, earnings are the most important driver of stock prices over the long run.