Wall Street's 2024 outlook for stocks 🔭

Plus a charted review of the macro crosscurrents 🔀

[UPDATE 12/18/23: For additional and updated 2024 targets and commentary, read this.]

Stocks climbed last week, with the S&P 500 rising 0.8% to close at 4,594.63. The index is now up 19.7% year to date, up 28.4% from its October 12, 2022 closing low of 3,577.03, and down 4.2% from its January 3, 2022 record closing high of 4,796.56.

It’s that time of year when Wall Street’s top strategists tell clients where they see the stock market heading in the year ahead. Typically, the average forecast for the group predicts the S&P 500 climbing by about 10%, which is in line with historical averages.

This year, strategists are offering a pretty wide range of views. Some see weakness. Some see strength. The targets range from 4,200 to 5,500. This implies returns between -8.5% and +19.7% from Friday’s close. For what it’s worth, the forecasts aren’t as skewed to the downside as they were last year.

Before we move on, I’d caution against putting too much weight into one-year targets. It’s extremely difficult to predict short-term moves in the market with any accuracy. Few on Wall Street have ever been able to do this successfully. I do however think the research, analysis, and commentary behind these forecasts can be informative.

That said, here’s what’s driving Wall Street’s views for 2024:

The economists that these stock market forecasters work with are split on whether the U.S. economy will go into recession some time during the year, which has implications for revenue among other things. Those who are expecting continued expansion expect growth to be modest, and those looking for a recession expect any downturn to be brief and shallow. (Scroll down for: Wall Street’s 2024 U.S. economic outlook 🇺🇸)

Interestingly, most strategists still expect S&P 500 earnings to grow in 2024 despite lackluster GDP growth forecasts. This may have to do with the expectation that consumer spending shifts back toward goods from services and the fact that the S&P has greater exposure to the goods sector, whereas U.S. GDP has greater exposure to the services sector.

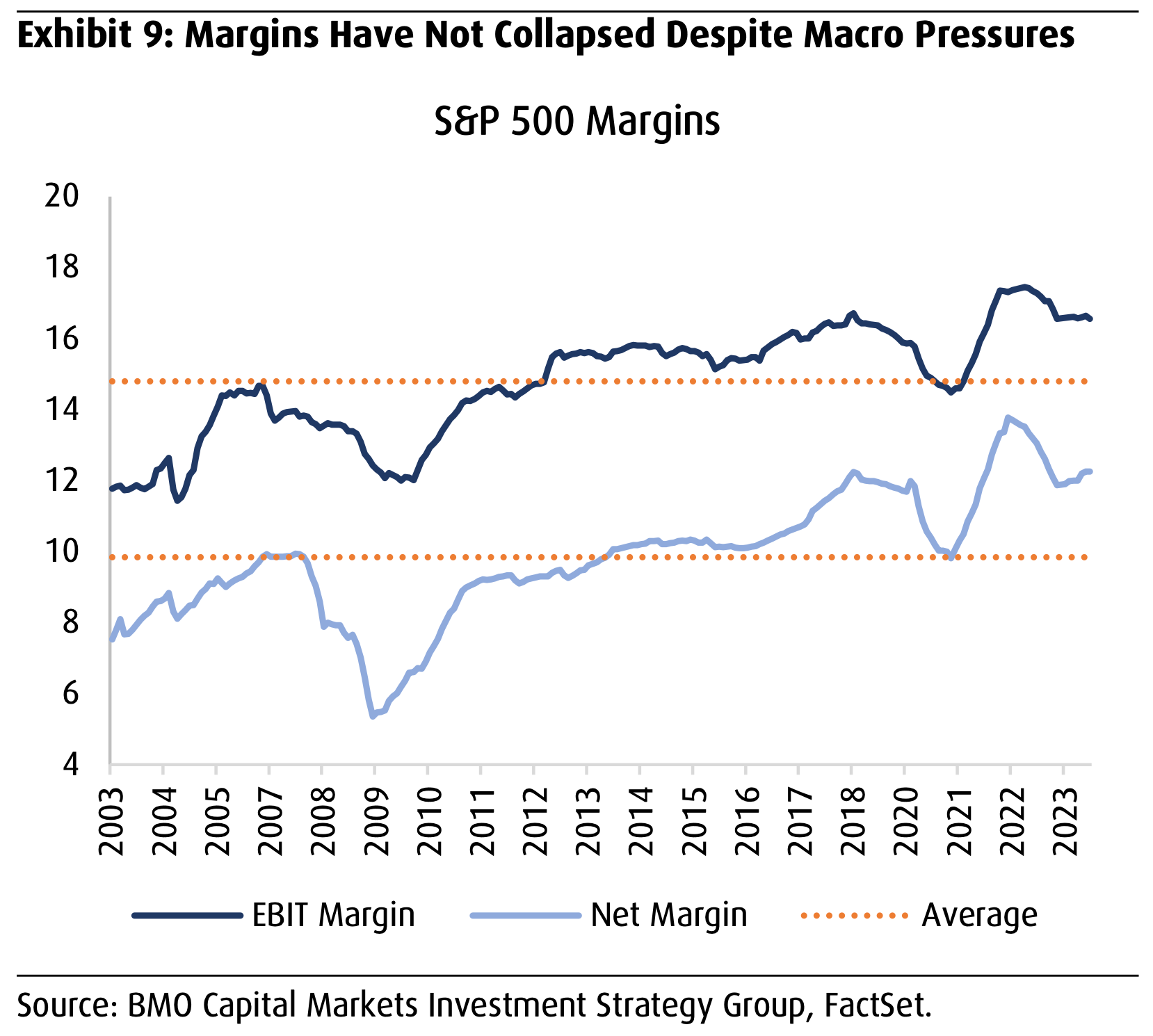

Analysts expect record earnings in 2024. (Source: FactSet) Thanks to improved operating efficiencies, many — but not all — strategists expect profit margins to stay high, which could help amplify earnings growth even with modest revenue growth.

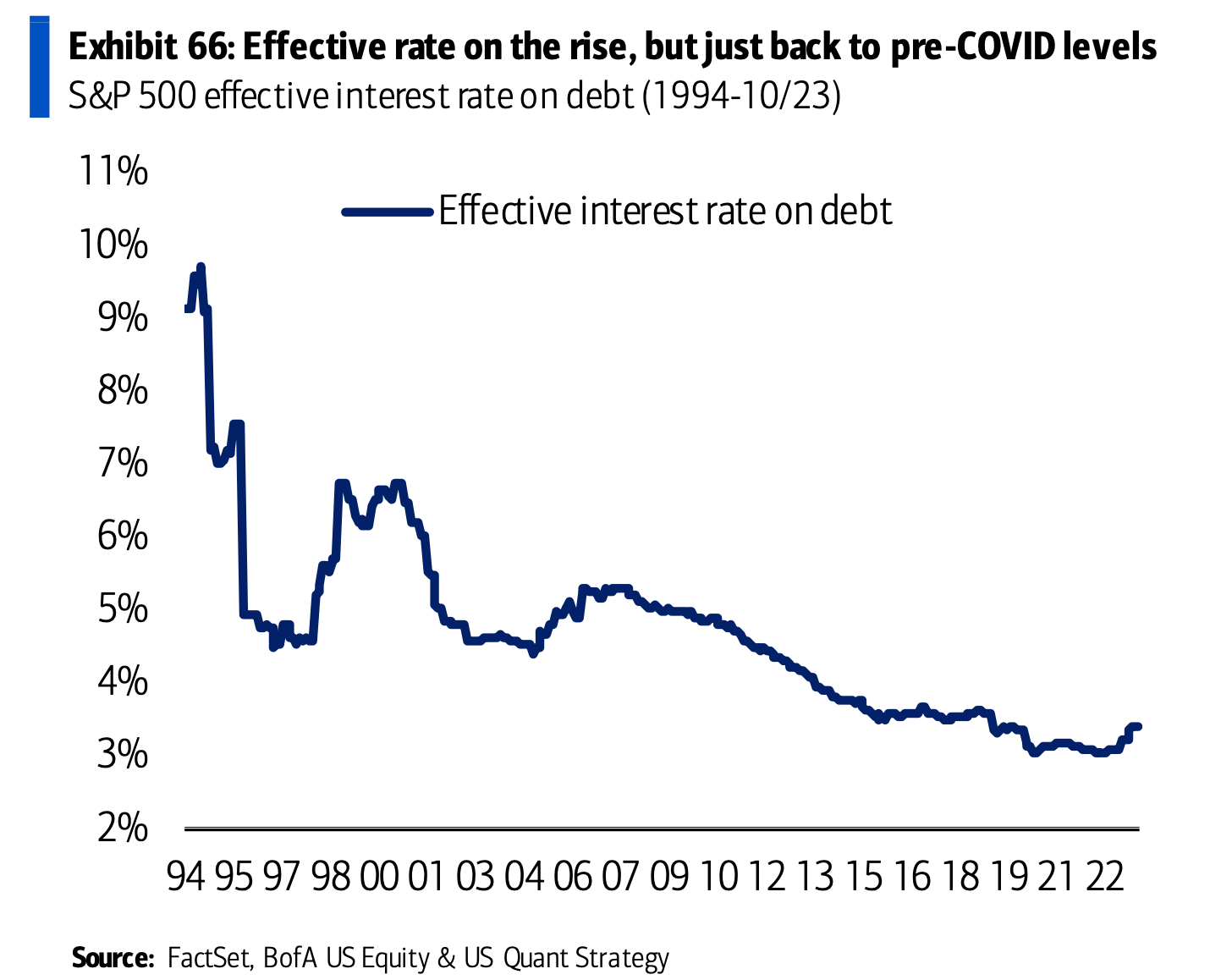

Profit margins have been holding up. (Source: BMO) While most S&P 500 companies have low interest rates on their debts locked in for years, more and more firms will still have to refinance at market rates, which continue to hover at their highest levels in years. Higher interest expense is a headwind for earnings growth.

Thanks to refinancing activity when rates were low, the interest large companies are paying remain low. (Source: BofA) Most strategists agree that the worst of the inflation crisis is behind us. This means that should economic conditions deteriorate significantly, the Federal Reserve may once again find itself loosening financial conditions with interest rate cuts. While an economic downturn would be unwelcome, it’s nevertheless good news that the Fed seems to have room to stimulate the economy.

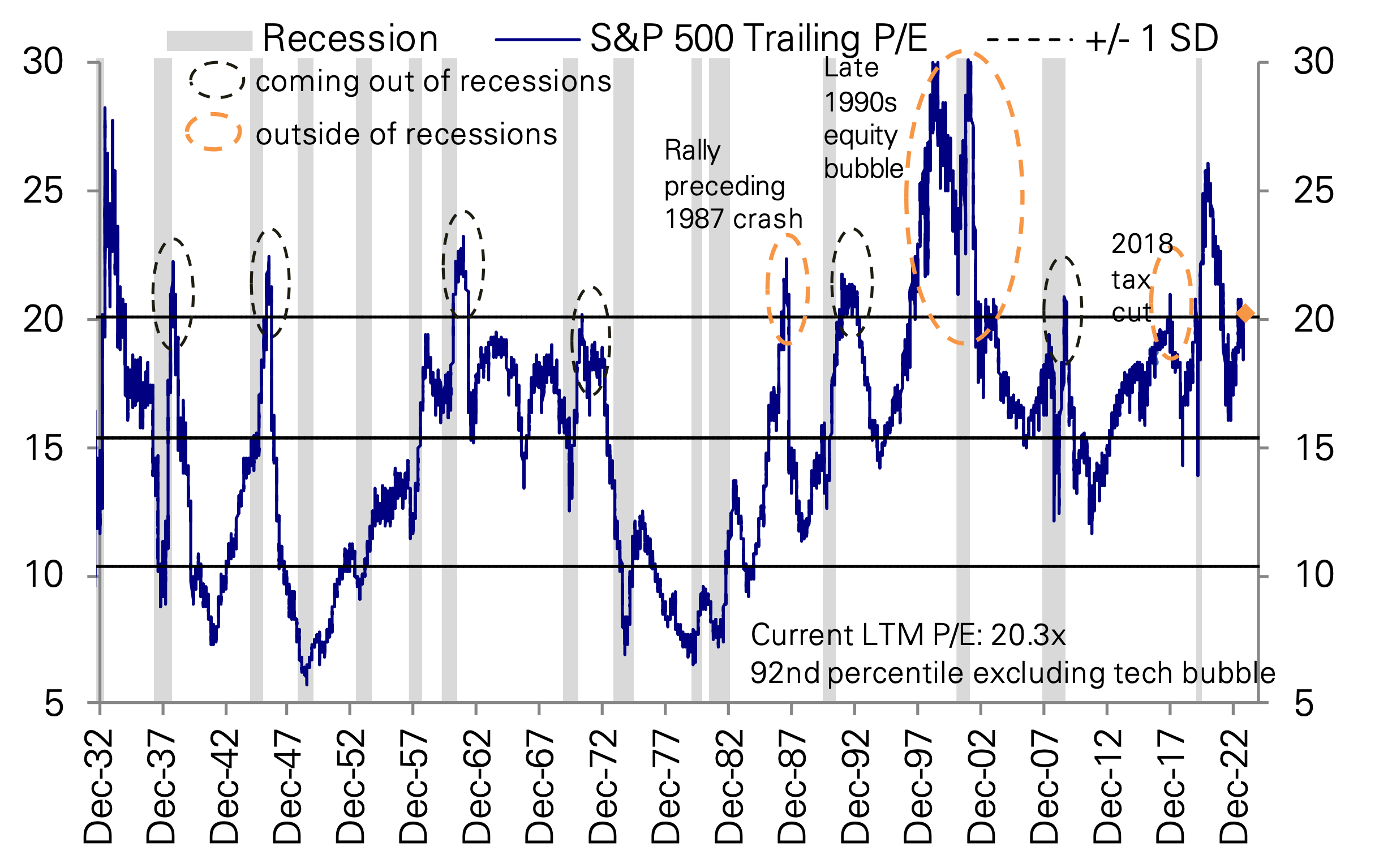

Strategists are also split on whether valuations are reasonable or whether they are a bit rich. This debate won’t go away anytime soon as valuations have historically signaled very little about short-term market moves.

While most strategist agree that valuations are elevated, not all believe that will prevent prices from going higher. (Source: Deutsche Bank) On valuations, at least one strategist argues that excitement for artificial intelligence technologies could persist into the new year, and the market could be in the early stages of a bubble.

The 2024 S&P 500 price targets 🔮

Below is a roundup of 12 of these 2024 forecasts for the S&P 500, including highlights from the strategists’ commentary.