Why repaying $500 can be harder than repaying $1,000 🤔

Any serious conversation about debt needs context 🧐

When I was in college, I didn’t make much money at my modest work-study job. It certainly didn’t earn me enough to pay off my credit card bill that one time I hit the $500 spending limit.

Terrified that I would never be able to come back from what looked like imminent financial ruin, I called my older sister for some one-time cash. It was humbling, but thankfully she bailed me out.

Today, as an actual adult with income, savings and a good financial plan, paying off a $1,000 credit card bill is a walk in the park. While the amount of credit card debt I carry may have doubled, my financial situation has completely changed.

Any serious conversation about debt of any nature — consumer debt, corporate debt, government debt — should also address the capacity to finance that debt.

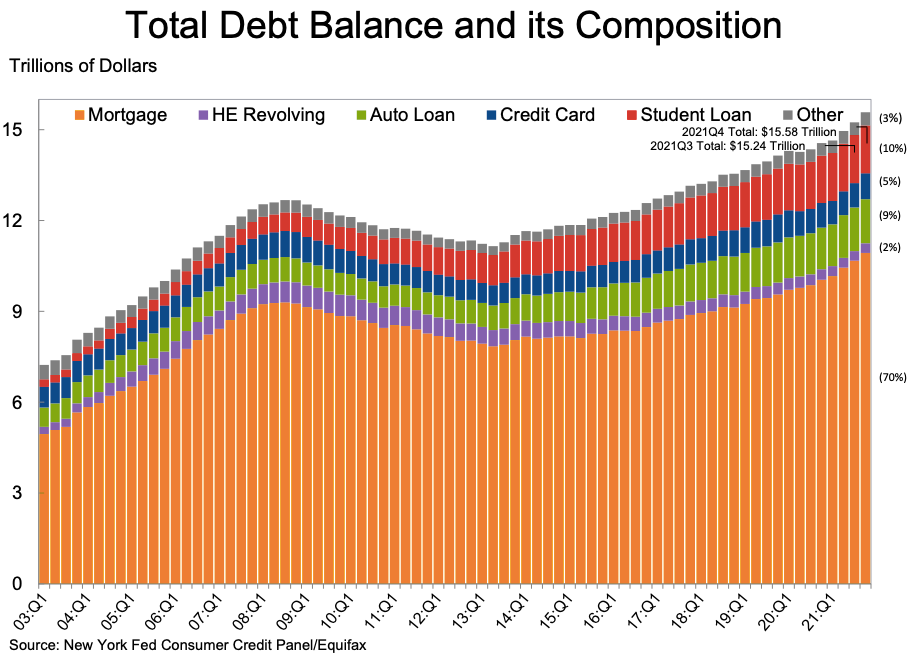

$15.58 trillion of consumer debt

You might’ve seen one of these headlines last week:

“U.S. Households Took On $1 Trillion in New Debt in 2021“ - The Wall Street Journal

“Consumer debt totals $15.6 trillion in 2021, a record-breaking increase“ - CNBC

“Household debt jumped by $1 trillion in 2021, the most since 2007“ - CNN

“U.S. household debt increased by $1 trillion in 2021, the most since 2007“ - Reuters

Every one of these headlines is accurate. They each draw from the NY Fed’s new quarterly household debt and credit report.

But if all you did was read the headline, you might think the accumulated debt is worrisome. After all, debt was at the heart of the financial crisis that brought down the economy 15 years ago.

A lot has changed over the years as debt levels have climbed. Consider the largest category of household debt: mortgages.

Mortgage balances increased to $10.93 trillion in the fourth quarter of 2021, up by $258 billion during the period. American households are carrying more mortgage debt today than they were during the height of the housing bubble.

However, there are two important pieces of context to note.

First, an overwhelming majority of new mortgages are going to borrowers with credit scores of 760 or higher, which is very high.

Second, there are indeed subprime mortgages being written (to those with a credit score of 620 or less). But the total value of originations for these borrowers is nowhere near where they were during the housing bubble of the 2000s.

The NY Fed’s report offers a lot of color on each of the categories of borrowing, including stats on delinquency and default rates. But the big takeaway is that borrowers generally have great credit quality and are mostly current on their financial obligations.

In a report to clients on Monday, Bank of America shared the two charts below showing that consumers (as well as businesses) have record levels of cash while their capacity to meet financial obligations has never been more robust.

Debt carries a negative stigma. But debt also enables people to buy a home 30 years before they have the cash. Debt allows young people to get the education that gets them on track for lifetime of higher earnings. Debt helps workers buy that car they need to get to that higher paying job.

Sure, too much debt can certainly put people (and businesses) at higher risk of going into financial ruin. However, “too much debt” should only be defined when you consider the borrower’s entire financial situation.

Some recent features from TKer:

Keep reading with a 7-day free trial

Subscribe to 📈 TKer by Sam Ro to keep reading this post and get 7 days of free access to the full post archives.