4 different ways of looking at the exact same economy 🪖👒🎩🧢

Plus a charted review of the macro crosscurrents 🔀

Stocks climbed last week, with the S&P 500 gaining 1.8% to close at 4,783.83. The index is now up 0.3% year to date, up 33.7% from its October 12, 2022 closing low of 3,577.03 and down 0.3% from its January 3, 2022 record closing high of 4,796.56.

Often times, those discussing what’s driving the stock market will appear in conflict with those discussing what’s driving the economy. And sometimes, those discussing what’s driving the economy will appear in conflict with each other.

These diverging views will happen even though everyone is in total agreement about the validity of the measurable data they’re citing.

How is this possible?

I think we can begin to disentangle what’s going on by thinking of people as wearing one of many different hats. There are at least four important hats that are worth a closer look.

The hard data economy hat 🪖

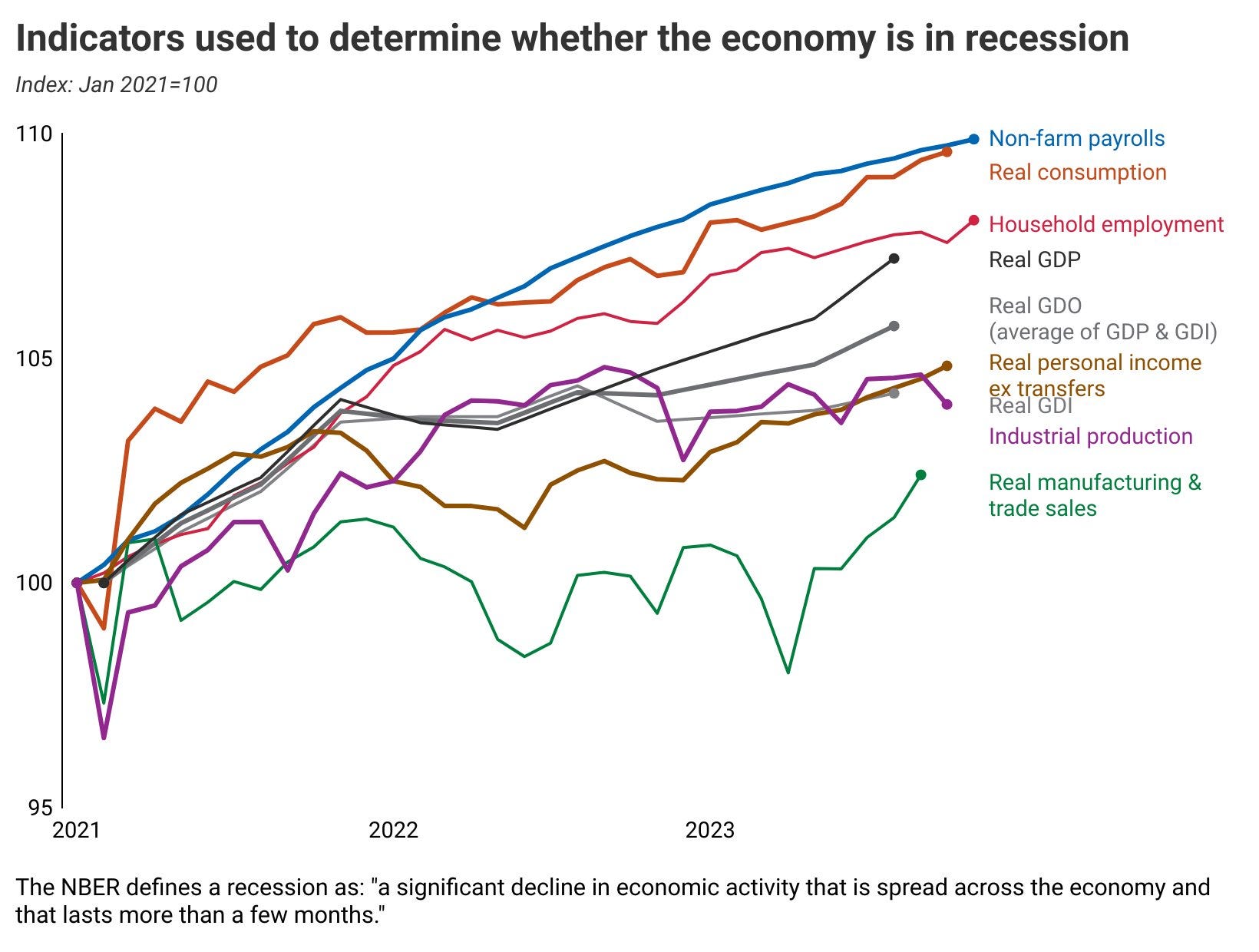

Hard data is anything that reflects quantifiable and observable behavior — stuff that is actually happening. Think job creation, wage growth, industrial output, retail sales, government spending, imports and exports, and consumer prices. There are receipts for all these things.

These include metrics that help us determine whether or not the economy is in expansion or recession.

We may actually need to divide this hat into two hats depending on how you measure economic activity. Some say the direction of the economy is reflected in two quarters’ worth of GDP, which relies strictly on monetary values of activity. Others go by the official NBER definition of activity, which considers non-monetary metrics like changes in employment.

While the GDP-oriented economy observers have perspectives that differ from the NBER-oriented observers, they at least agree that the activity is based on hard measures. It’s just a matter of how they weight those measures.

Generally speaking, hard data metrics have been favorable — mostly reflecting a growing economy.

For more, read: The economy has gone from very hot to pretty good 😎 and You call this a recession? 🤨

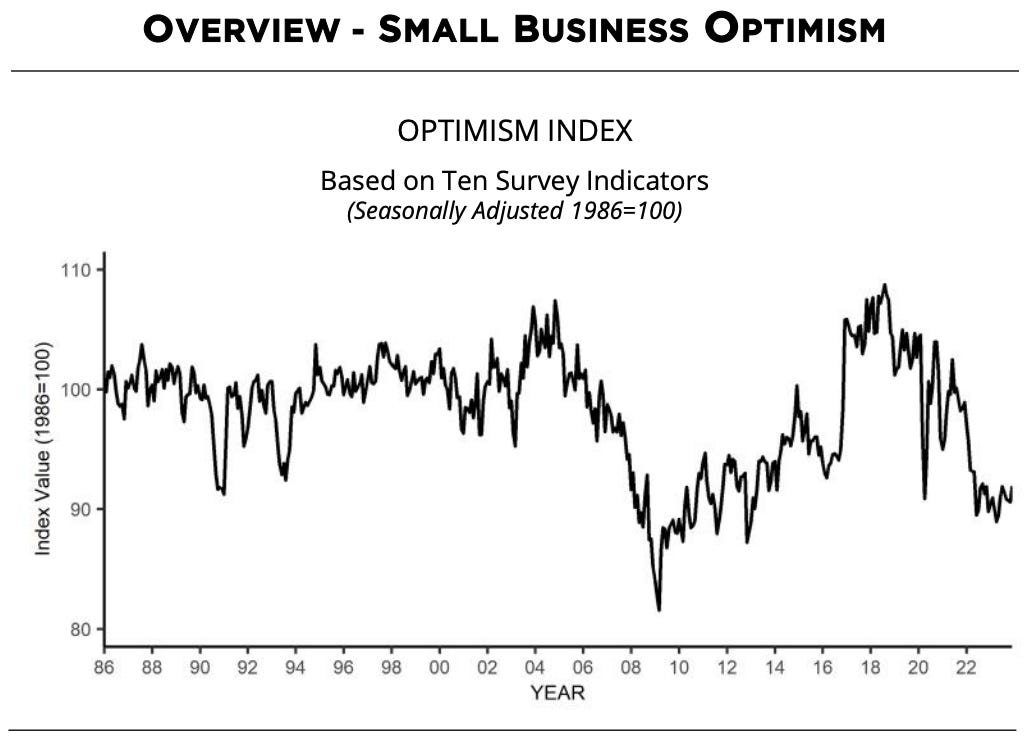

The soft data economy hat 👒

Soft data is generated through surveys of consumers and business operators expressing their opinions, feelings and expectations about things like job security, financial health, inflation, future business activity, and labor quality. They’re measurements of stuff people feel is happening or feel will happen.

Popular reports capturing soft data include the New York Fed’s Survey of Consumer Expectations, the ISM’s Manufacturing PMI, the NFIB’s Small Business Optimism Index, and the University of Michigan’s Surveys of Consumers.

Soft data reflect the vibes, as Kyla Scanlon would say.

Recently — despite robust hard economic data — the economic vibes haven’t been great, as consumer and business sentiment have spent most of the past two years in the dumps.

Does this mean we should dismiss the sentiment data?

Of course not.

What good is it to have lots of money and to buy everything you want if you’re more unhappy than you were when you had less money and less stuff?

For more, read: A bullish contradiction 🛍 and What businesses do > what businesses say 🙊

The stock market hat 🎩

In the short run, news about the hard and soft economic data can move the stock market. Technical factors in the markets will also move prices in the near term. Pretty much anything you imagine can affect trader decisions and investor sentiment, which in turn affects the markets over short periods of time.

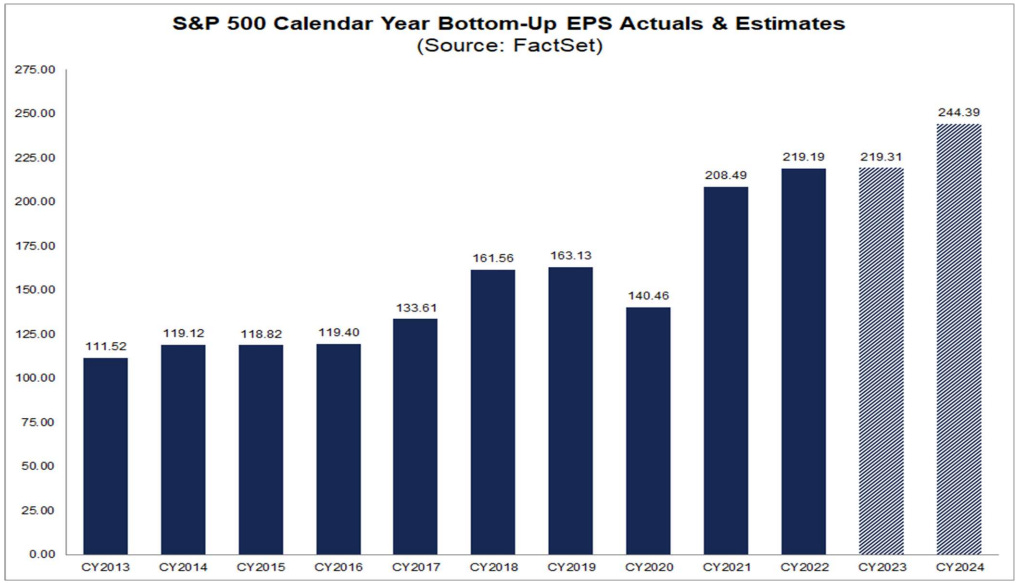

But in the long run, the most important driver of stock prices is earnings.

As I explained in TKer Stock Market Truth No. 2, “News about the economy or policy moves markets to the degree they are expected to impact earnings. Earnings (a.k.a. profits) are why you invest in companies.“

When thinking about stocks over the long term, soft economic metrics matter to the degree they affect hard economic metrics. And hard economic metrics matter to the degree they affect earnings.

This can get complicated, because it’s certainly possible to have economic recessions that aren’t associated with earnings recessions.

As explained in the Nov. 29 TKer, 2024 could be a year when the stock market performs considerably better than the economy due to contrasting exposures to the goods and services sectors. Improving economic metrics won’t always coincide with improving earnings, and vice versa.

Earnings, for their part, have been trending higher and are expected to keep going higher, which helps explain why stock prices are near record highs. Analysts expect double-digit earnings growth in 2024 and 2025.

And when earnings are going up, the stock market usually goes up.

For more, read: Earnings are the most important driver of stock prices💰

The biased hat 🧢

Unfortunately, there are many people and entities who are unable to look at data objectively. And so whatever the development may be, they’ll figure out a way to spin it so the story confirms their priors.

This is often the case for permabears, who’ll spin anything negatively, and permabulls, who’ll spin anything positively.

There are also some business news reporters and outlets who are more concerned about getting clicks and engagement on their stories than they are about reporting the data fairly. And so while the balance of data may be favorable, you may get outsized coverage of unfavorable cherry-picked data if it attracts reader interest.

Political persuasions can play a huge role in how people view data. If you’re in office and you’re looking to get re-elected, then you’ll probably spin developments in your favor. If you’re not in office but seeking to get elected, then you’ll have an incentive to spin the data unfavorably so the incumbent looks bad.

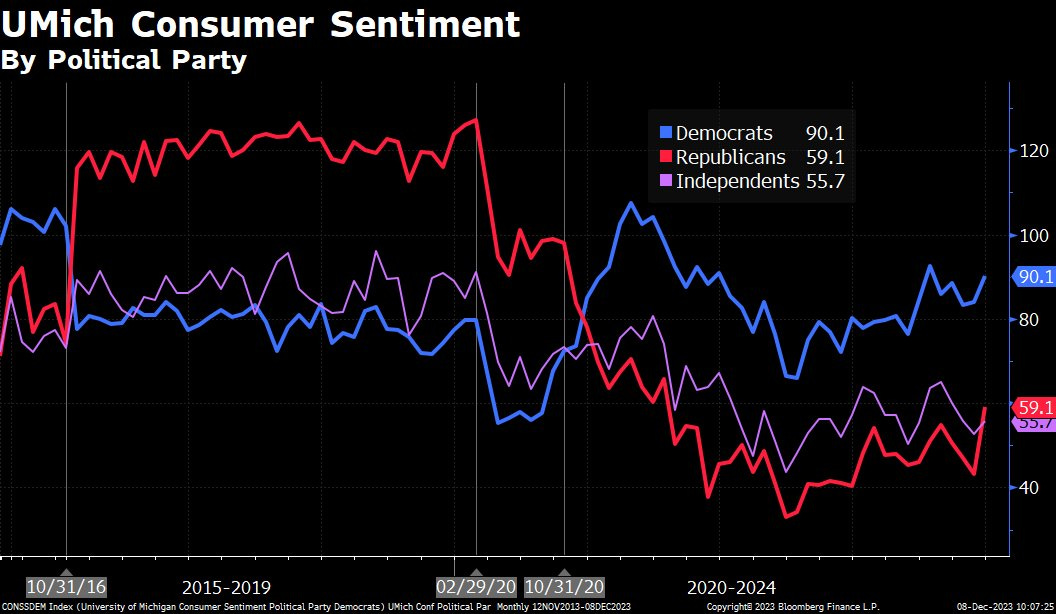

As the University of Michigan’s consumer sentiment data shows, views on the economy contrast considerably depending on political affiliations.

To be fair, biased views and balanced views aren’t totally mutually exclusive. In many cases, their conclusions may be in line.

But in other cases, biased folks will turn a blind eye to developments that undermine their priors, and that can be dangerous for anyone listening.

Beware the motivations of those communicating information.

Fore more, read: 11 ways cynics argue any news is bad news 👎, A 5-step guide to processing ambiguous news 📋, Is good economic news really all that surprising? 📰, and Beware alarming business stories that get a lot of news coverage 🗞️

Zooming out 🔭

So, how’s the economy?

Well, it depends on whom you ask.

The hard data folks will likely tell you the economy is growing, but it appears to be cooling. Many warn a recession could be around the corner.

The soft data folks will probably tell you the economic vibes aren’t good, but there are signs they’re improving.

The stock market folks might tell you economic growth may be cooling — but in a way that should allow big companies to report healthy earnings growth, which should help send stock prices higher.

However Democrats feel, you can bet Republicans feel worse.

Each group may have different tones, but they’re not necessarily in disagreement about the measurable data.

FULL DISCLOSURE: TKer tends to wear the stock market hat.

-

Related from TKer:

Reviewing the macro crosscurrents 🔀

There were a few notable data points and macroeconomic developments from last week to consider: