Taming my 'big dumb lizard brain' with a 'cowboy account' 🦎

Plus a charted review of the macro crosscurrents 🔀

📉 The stock market declined, with the S&P 500 falling 1.5% last week to close at 5,580.94. It’s now down 9.2% from its February 19 closing high of 6,144.15 and up 56% from its October 12, 2022 closing low of 3,577.03. For more on market moves, read: Investing in the stock market is an unpleasant process 📉

-

Something I love about Barry Ritholtz’s writing is how he often surprises you with unexpected insights.

Sure, he advances well-known — but still underappreciated — wisdom like how index fund investing is hard to beat and why making short-term market forecasts is futile.

But he offers much more than that.

Take this excerpt on psychology from his new book, “How Not To Invest,” which he shared in a recent piece for Bloomberg:

Trick Your Lizard Brain

Nobel laureate Paul Samuelson once said, “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” While the dopamine hit that comes from a risky stock bet paying off may be enjoyable, passive management is the better option for most investors looking to grow long-term wealth.

The catch is that you must take steps to protect yourself from, well, yourself. To do so, set up a “mad-money account” — or a cowboy account, as it’s sometimes called. Add less than 5% of your liquid capital, so maybe $5,000 if you’re liquid enough to have $100,000 as a safety net. Now you can indulge your inner hedge fund manager without jeopardizing anything too material.

If it works out, you’re more likely to let those winners run because it’s for fun and not your real money. If it’s a debacle, appreciate the terrific lesson that should remind you that this is not your forte.

In his book, Barry shares a little more on what he personally does:

In my cowboy account, using 2% of my liquid net worth, I play the dumbest game possible: Market timing with out-of-the-money stock option calls…

He discusses specific trades he’s made. I’ll let you buy the book if you really want the details.

Here’s his bottom line.

Regardless of the results, it allows my inner junkie to leave my main portfolio alone. That is the true value of the cowboy account — my real money remains unmolested by me and my big dumb lizard brain.

Like most of us, Barry is not a machine. He is a human with a brain. And when your brain is mismanaged, it can be your worst enemy.

The idea of having a “cowboy account” is not without its issues. Some of you might say it could be a slippery slope towards costlier risk taking. This advice certainly isn’t for everybody. But let’s also not pretend like living in denial of your instincts and biases isn’t risky either.

As TKer subscribers know, my investing mostly consists of buying and holding passively managed index funds. But while I may have lost my taste for picking stocks and timing the market a long time ago, I haven’t lost my appetite for risk.

Personally, I’ve taken Samuelson’s advice much more literally. Occasionally, I like to play craps live in a casino. That’s the game where you often hear crowds of people cheer loudly as they engage in the mania of a “hot” table. I won’t get into too much detail, but it’s a game where I can lose enough that it’s memorably painful but not so much that it’s material to my finances. Importantly, it satiates my risk appetite, and it gives me renewed appreciation for my financial plan at relatively low cost.

In some ways, investing is like dieting: For many people, attempting to cut out junk food entirely just doesn’t work.

If you want to learn more about how real people can better navigate the treacherous world of investing, buy Barry’s book. He’s got real world solutions for your real world challenges.

For more info, head to HowNotToInvestBook.com »

-

Related from TKer:

Most stock-picking pros underperformed in 2024's market rally 🫤

Warren Buffett reminds us how picking winning stocks is hard 🤓

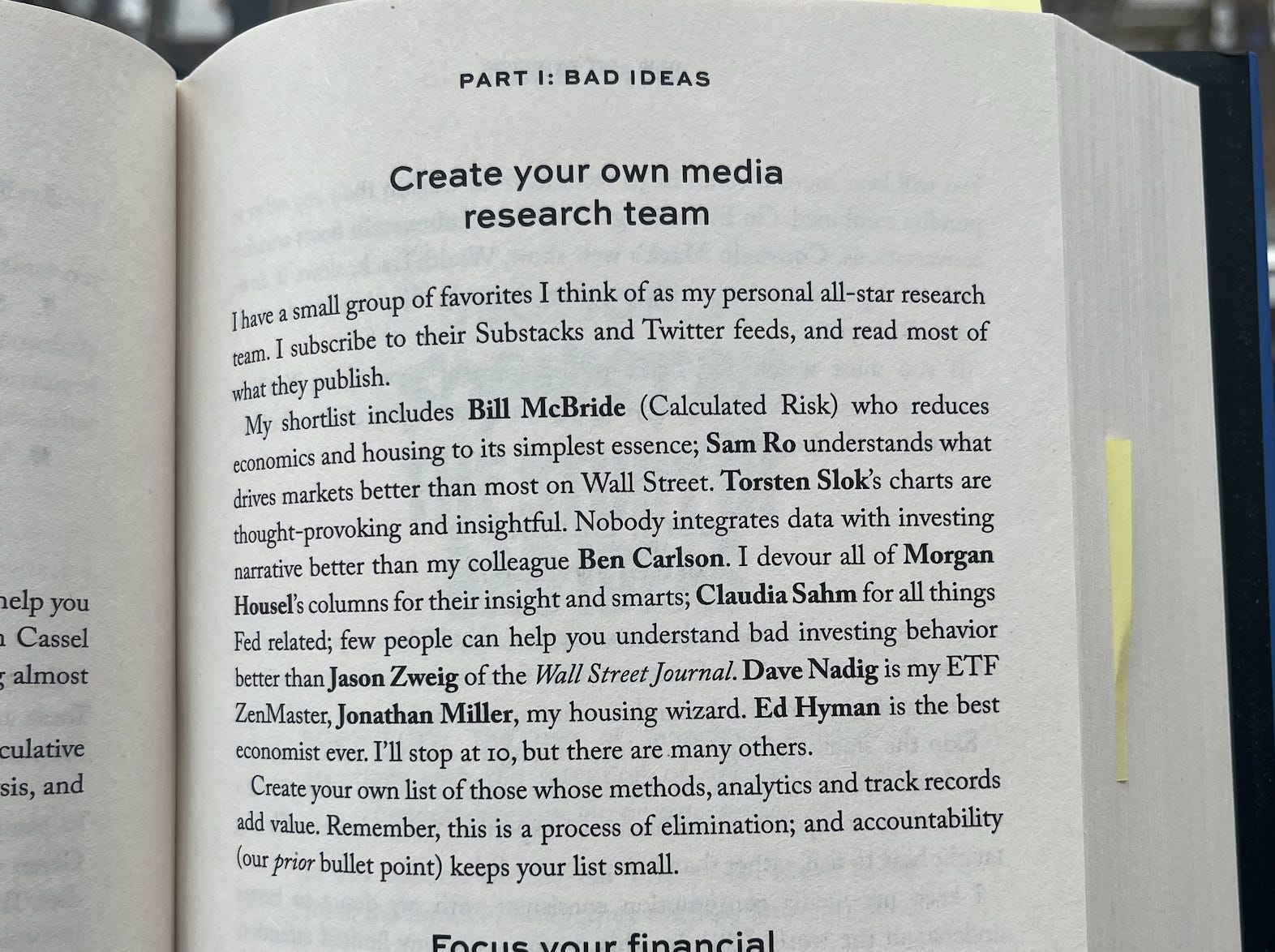

📘 Sam Ro mention!

I was shocked and humbled to learn that Barry mentioned me in “How NOT To Invest.” I’ve been reading his blogs since before the financial crisis. He’s had a huge impact on how I think and write about markets.

If you like TKer, then you’ll love Barry’s writing. Catch up on his views by reading his book!

Listen up! 🎧

I was on The Compound & Friends podcast on Thursday with Andrew Beer of Dynamic Beta Investments, the legendary Josh Brown, and the brilliant Michael Batnick. We covered a lot. Trump trade policy, stock market sentiment, credit, hedge funds, diversification, and more! Listen on Apple Podcasts, Spotify, YouTube, and beyond!

Review of the macro crosscurrents 🔀

There were several notable data points and macroeconomic developments since our last review: