What comes after the bubble could be electrifying ⚡️

Plus a charted review of the macro crosscurrents 🔀

📈The stock market rallied to all-time highs, with the S&P 500 setting an intraday high of 7,002.28 on Wednesday and a closing high of 6,978.60 on Tuesday. The index ended the week at 6,939.03 and is now up 1.4% year-to-date. For market insights, check out the Stock Market tab at TKer. »

-

If AI is all it’s cracked up to be, the winners in the stock market should extend far beyond the large-cap tech hyperscalers currently building the AI infrastructure.

As BofA’s Savita Subramanian wrote back in June 2023: “The larger benefit may be had by old-economy, inefficient companies that can increase earnings power more permanently from efficiency and productivity gains.”

It’s too early to say conclusively, but the market may be in the process of getting in front of this phase of the AI narrative, as small-cap stocks have recently been outperforming large-cap stocks.

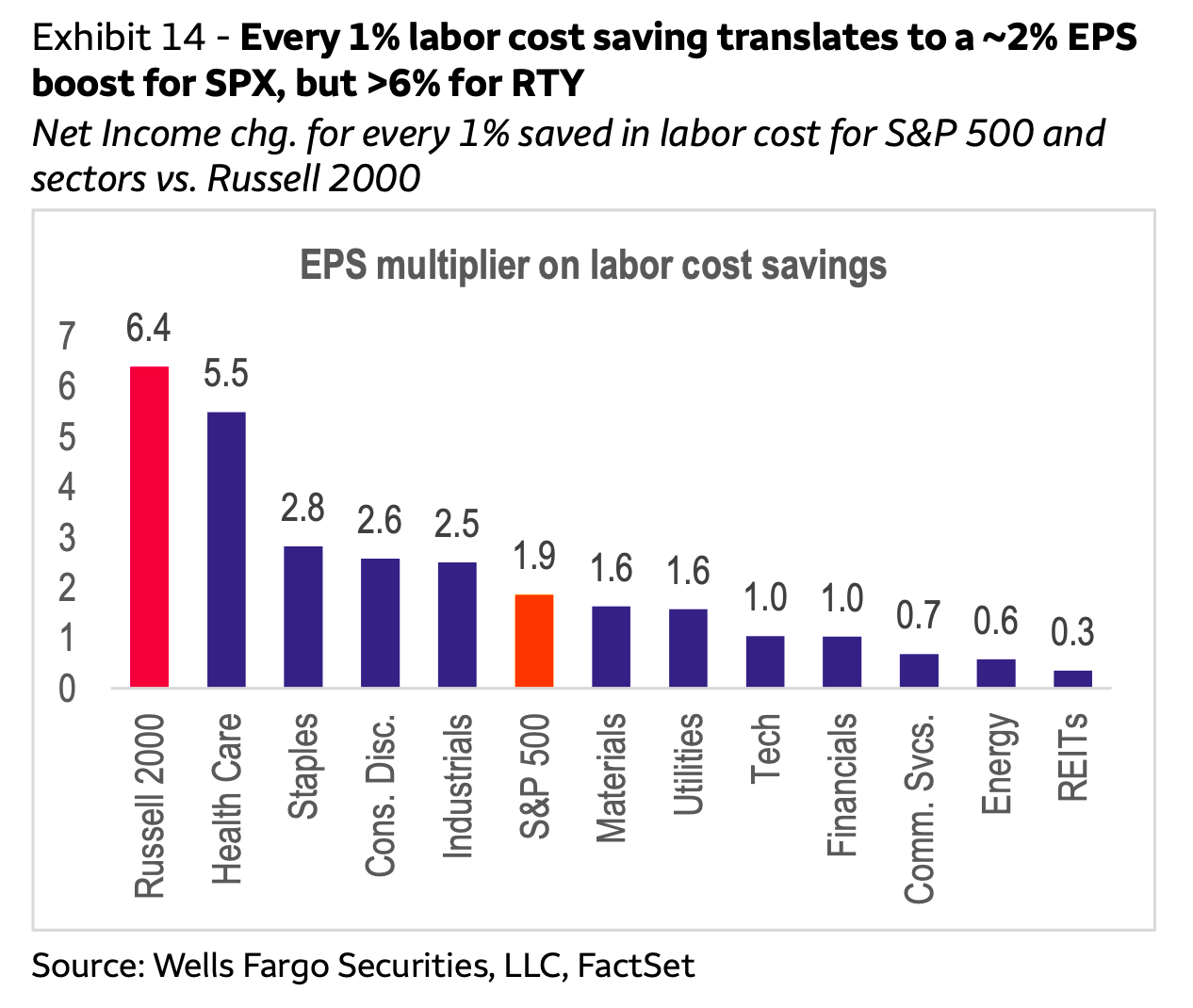

As Wells Fargo’s Ohsung Kwon argues, small-cap stocks (as tracked by the Russell 2000, or RTY) could see a bigger tailwind from AI than large-cap stocks (as tracked by the S&P 500 or SPY).

“We see signs that small caps have been slower to adopt AI than large caps,” Kwon wrote on Monday. “We believe the next leg of AI adoption is in small caps — the longer-term bull case for RTY. We estimate every 1% labor cost saving translates to a ~2% EPS boost for SPX, but >6% for RTY.”

This is what makes the promise of AI truly exciting for investors: The beneficiaries aren’t limited to those developing the technology. Companies across industries have been exploring AI applications, and many are already implementing them in their operations.