Income and costs affect you and your neighbors differently 💵

Plus a charted review of the macro crosscurrents 🔀

A $4 gallon of gas or an extra $1,000 of income means different things to different people.

Most drivers notice when the price of a gallon of gas goes up by a dollar. But those earning high income don’t feel the pinch quite like those earning low income.

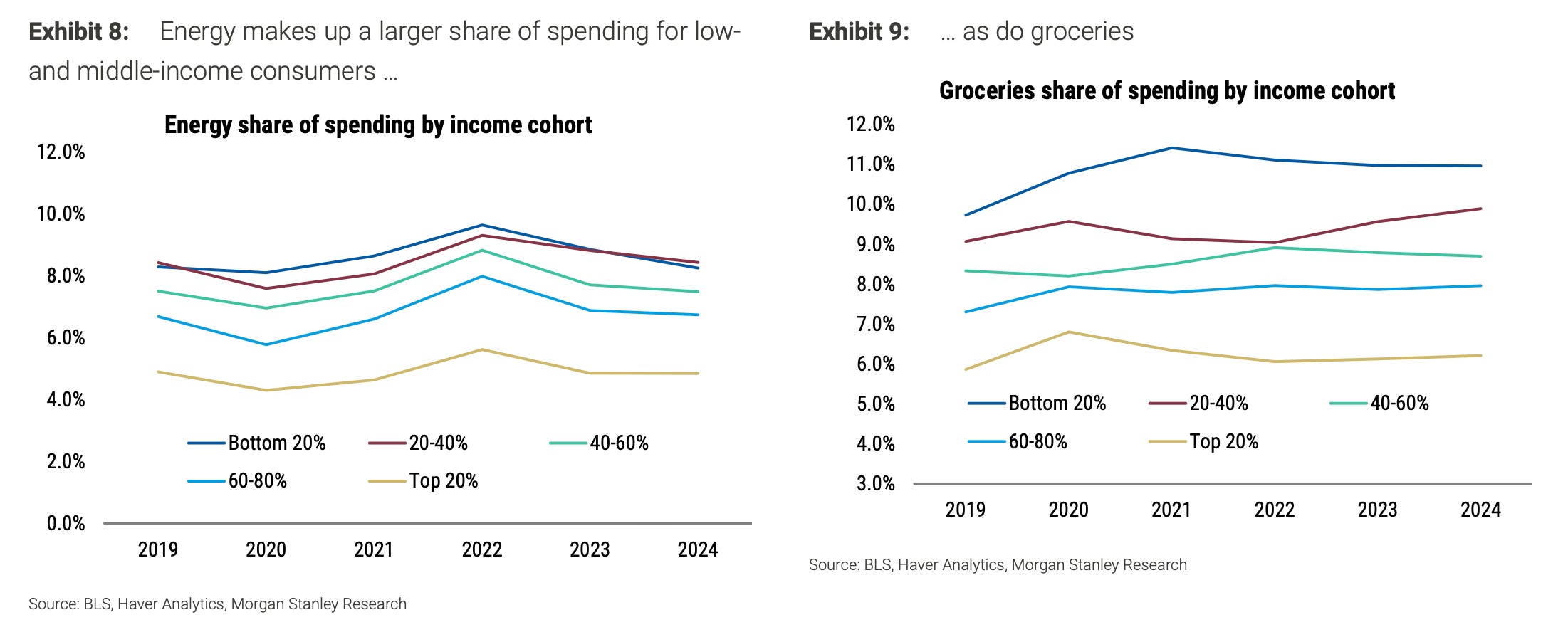

“For low-income consumers, spending on essentials, including energy and food, is a larger share of both their total spending and their income,” Morgan Stanley economists wrote last month. “As of the most recent Consumer Expenditure Survey from 2024, energy spend made up 8.2% of total spending for the bottom 20% income cohort compared to 4.8% for the top. Limiting to just gasoline, gas made up 3.6% for the bottom cohort versus 2.6% for the top.”

Furthermore, fiscal policy affects consumers differently depending on their income level. It usually benefits those at the bottom — but that is not currently happening.

“[We] do not expect the lowest-income cohort (bottom 10-20%) to benefit much from the fiscal bill this year,” the economists added. “Much of this low-income cohort already does not pay federal income taxes because of other credits and deductions, and therefore cannot benefit from the new tax provisions. Meanwhile, some of the spending cuts in the fiscal bill start to ramp up this year, including cuts to SNAP benefits and Medicaid. This will hurt some consumers in that low-income group.”

As a result, the economists expect us to keep hearing about the “K-shaped” narrative, which explains how the economy is being bolstered by wealthier, higher-income folks as they do better while poorer, lower-income folks do worse.

Marginal propensities to consume 🛒

Investors sometimes take the K-shaped dynamic for granted, because revenue is revenue regardless of who’s spending. And if revenue is holding up and earnings are growing, what’s the big deal?

Well, it’s somewhat well-known that if you give two people checks for the same amount of money, the poorer person is likely to spend more of that check right away than the richer person.

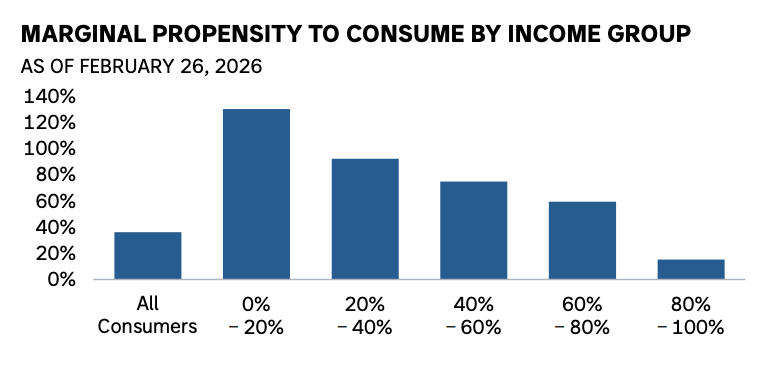

Morgan Stanley’s Lisa Shalett discussed this in November: “Much has been made about higher-income cohorts driving a larger share of spending, given wealth effects. That said, on the margin, it remains the lower income cohorts that can impact annual growth of consumption the most, as their marginal propensity to spend an incremental dollar of earnings is more than six times more impactful than that of the wealthiest cohort. On this point, the 2026 outlook is increasingly fragile.“

An incremental dollar of earnings can improve a low-income person’s standard of living materially, whereas that same dollar may do little for someone whose living standards are already high.

So, the low-income person is more likely to spend that dollar instead of saving it. This is why economists often argue that fiscal policy favoring low-income folks can have a more immediate stimulative effect on the economy.

The big picture 🖼️

In the context of the stock market, we’ve mostly talked about the consumer as a monolith that has been in a healthy financial position.

Because while the retailer or the airline or the restaurant may talk about how customer mix and spending behavior are shifting between demographics, from a financial perspective, it doesn’t matter if it’s a high-income or low-income customer who’s spending. Spending is spending.

The economy is complicated. Familiarizing yourself with the many nuances of demographics can help you better understand how the economy functions, why it will behave in counterintuitive ways, and how policy can affect it.

-

Related from TKer:

The economy may not be working for everyone right now, but it’s working for stock market investors 🎭

Watch 📺 and Listen🎧

I was on Full Disclosure with Roben Farzad. Roben is an absolute legend. We talked about how I got into writing about markets, my experience becoming an independent publisher, and why it’s so tough to beat the market. Check it out on YouTube or anywhere you get podcasts!

I joined my long-time colleague and friend, Myles Udland, on Yahoo Finance. We talked about market volatility, the Magnificent 7’s pullback, earnings, and financial media. Check it out on YouTube!

I was also on Facts vs Feelings: Social Hour with Ryan Detrick, Sonu Varghese, and Frank Cappelleri. We talked about geopolitics, oil, monetary policy, the role of diversification in portfolios, and the evolution of the Predator movie franchise. Catch it on Spotify or YouTube!

Review of the macro crosscurrents 🔀

📈The stock market climbed last week, with the S&P 500 gaining 3.4% to end at 6,582.69. The index is now down 5.7% from its Jan. 27 closing high of 6,978.60 and down 3.8% year-to-date. For market insights, check out the Stock Market tab at TKer. »

There were several notable data points and macroeconomic developments since our last review:

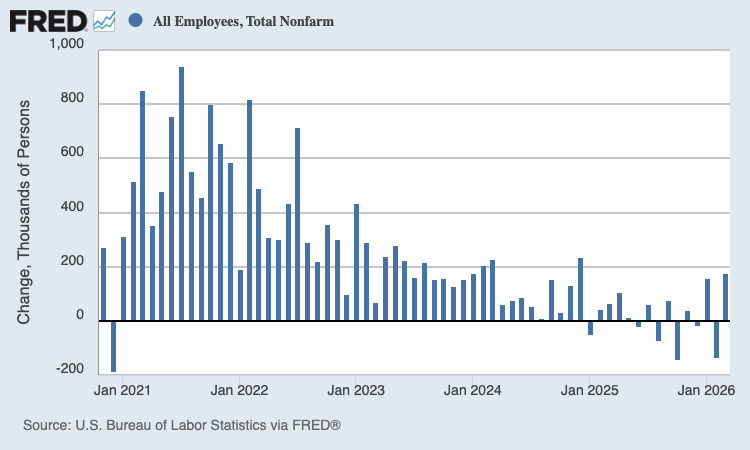

💼 Jobs were created. According to the BLS’s Employment Situation report released on Friday, U.S. employers added 178,000 jobs in March. This metric has been noisy in recent months, going negative in five of the last ten months.

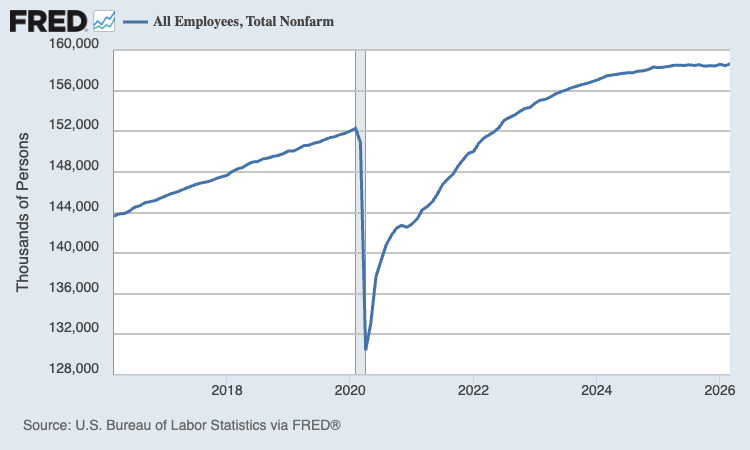

Total payroll employment rose to a record 158.6 million jobs in March.

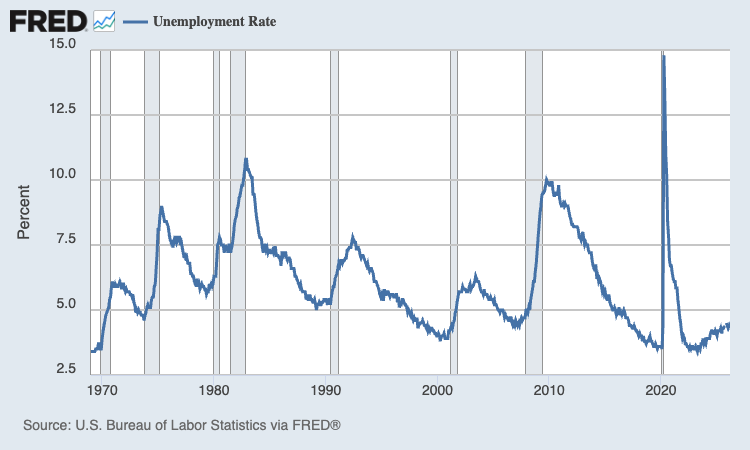

The unemployment rate — that is, the number of workers who identify as unemployed as a percentage of the civilian labor force — declined to 4.3% in March.

The labor market clearly isn’t as hot as it used to be.

For more on the labor market, read: About that ugly Feb. jobs report 📉 and We’re at an economic tipping point ⚖️

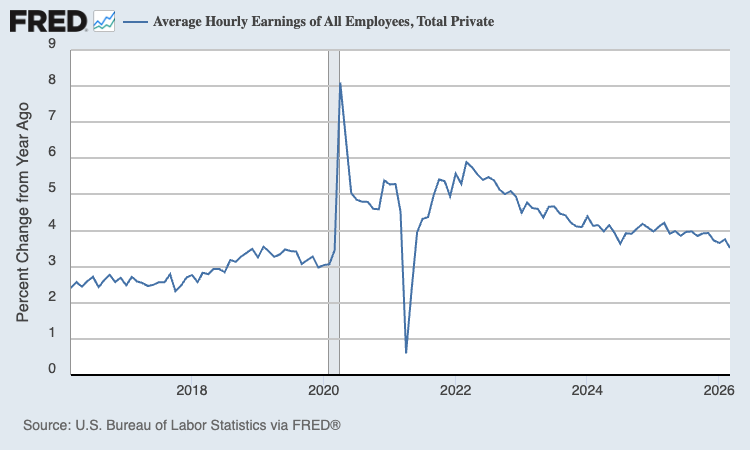

💸 Wage growth cooled. Average hourly earnings rose by 0.2% month-over-month in March. On a year-over-year basis, March’s wages were up 3.5%, the lowest level since May 2021.

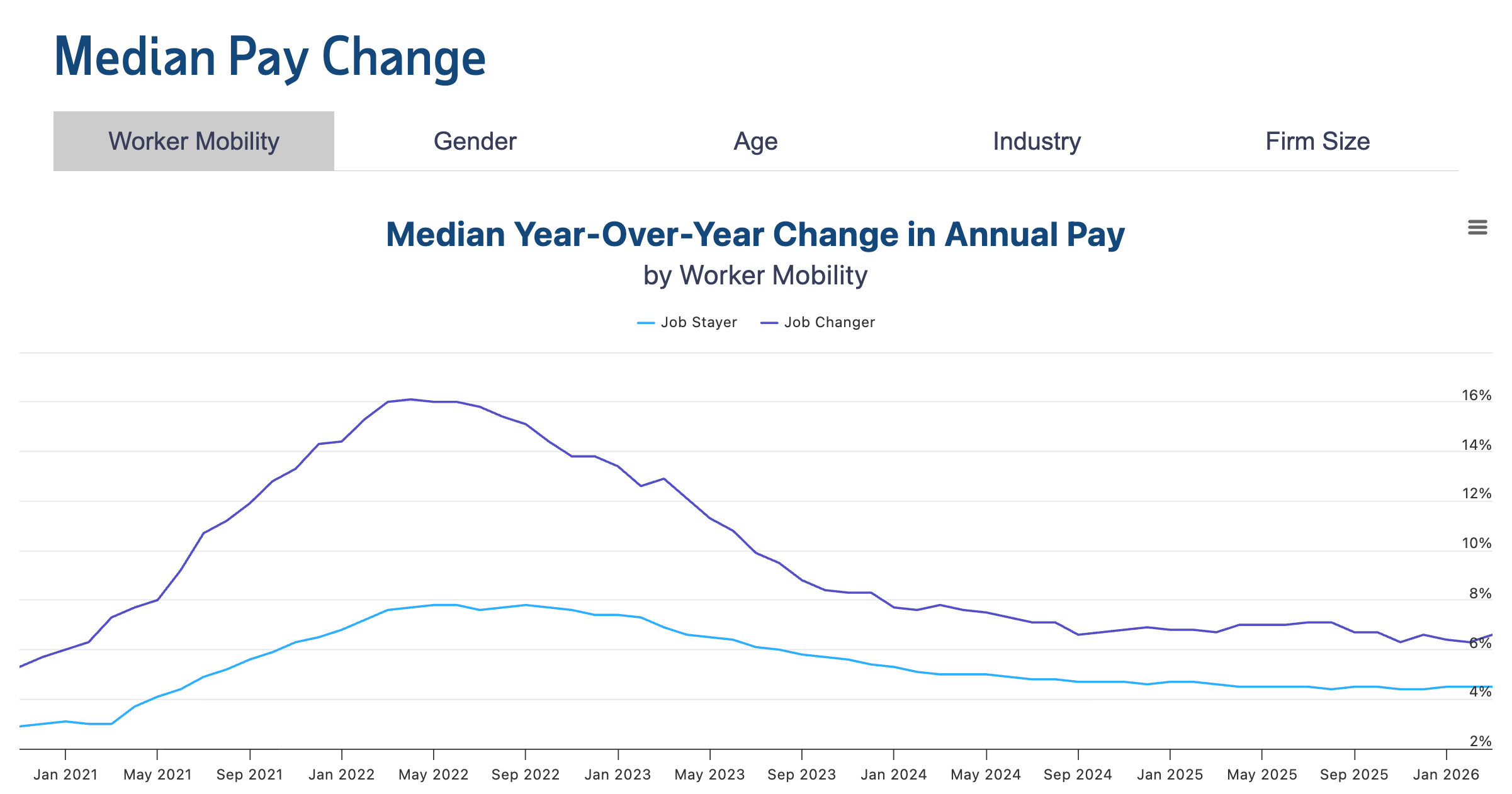

💰 Job switchers still get better pay. According to ADP, annual pay in March for people who changed jobs was up 6.6% from a year ago. That better-pay gap has been cooling a bit in recent months. For those who stayed at their job, pay was up 4.5%, about what it’s been for the past year.

For more on why policymakers are watching wage growth, read: Revisiting the key chart to watch amid the Fed’s war on inflation 📈

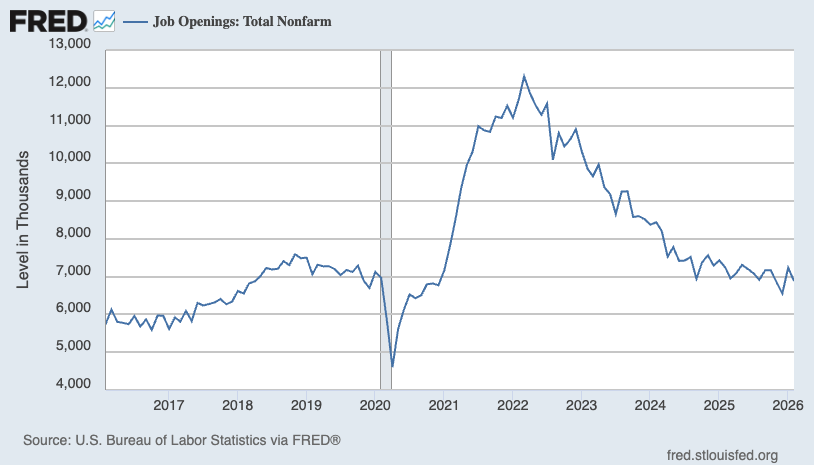

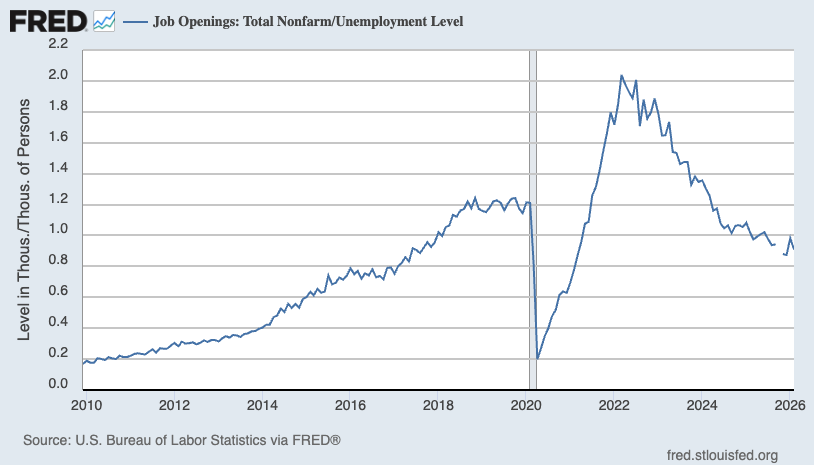

💼 Job openings fall. According to the BLS’s Job Openings and Labor Turnover Survey, employers had 6.88 million job openings in February, down from 7.24 million in January.

During the month, there were 7.57 million unemployed people — meaning there were 0.91 job openings per unemployed person. This remains one of the most straightforward indicators of labor demand. However, this metric has returned to prepandemic levels.

For more on job openings, read: Were there really twice as many job openings as unemployed people? 🤨 and Revisiting the key chart to watch amid the Fed’s war on inflation 📈

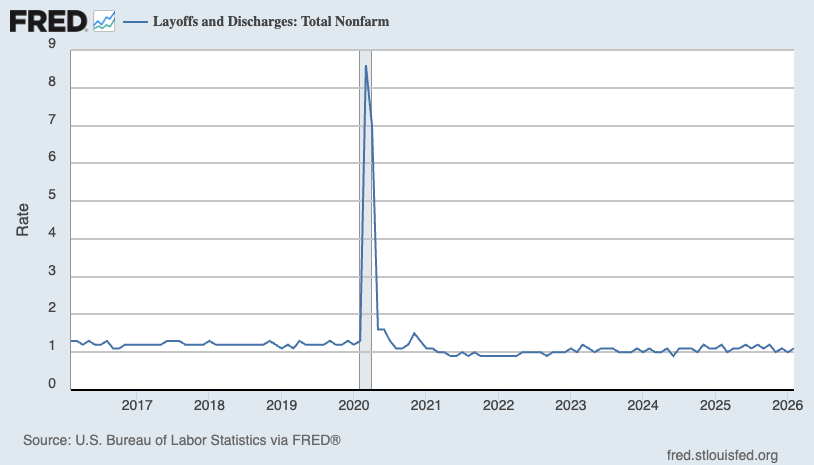

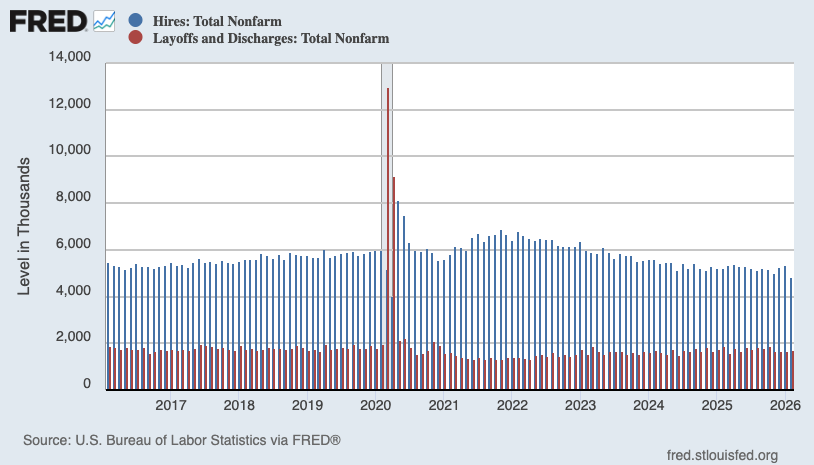

👍 Layoffs remain depressed, hiring remains firm. Employers laid off 1.72 million people in February. While challenging for the people affected, this figure represents just 1.1% of total employment. This metric remains slightly below prepandemic levels.

For more on layoffs, read: Mathematical context can totally change the story 🧮

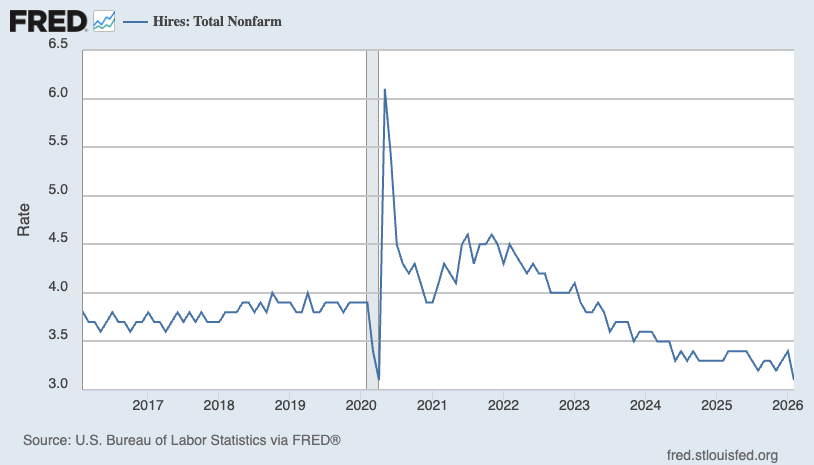

Hiring activity remains well above layoff activity. During the month, employers hired 4.85 million people.

That said, the hiring rate — the number of hires as a percentage of the employed workforce — has been trending lower, which could be a sign of trouble to come in the labor market.

For more on why this metric matters, read: The hiring situation 🧩

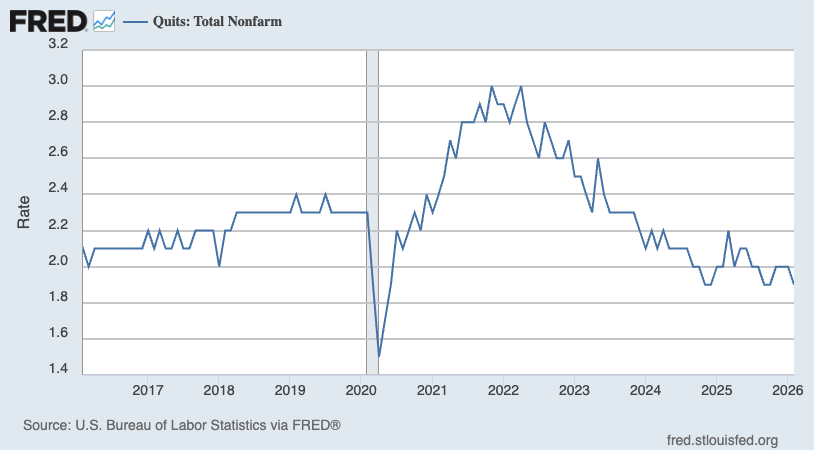

🤔 People are quitting less. In February, 2.97 million workers quit their jobs. This represents 1.9% of the workforce. The rate continues to trend below prepandemic levels.

A low quits rate could mean a number of things: more people are satisfied with their job, workers have fewer outside job opportunities, wage growth is cooling, or productivity will improve as fewer people are entering new, unfamiliar roles.

For more on this dynamic, read: The crummy labor market is yielding a ‘tenure dividend’ for corporations 💰

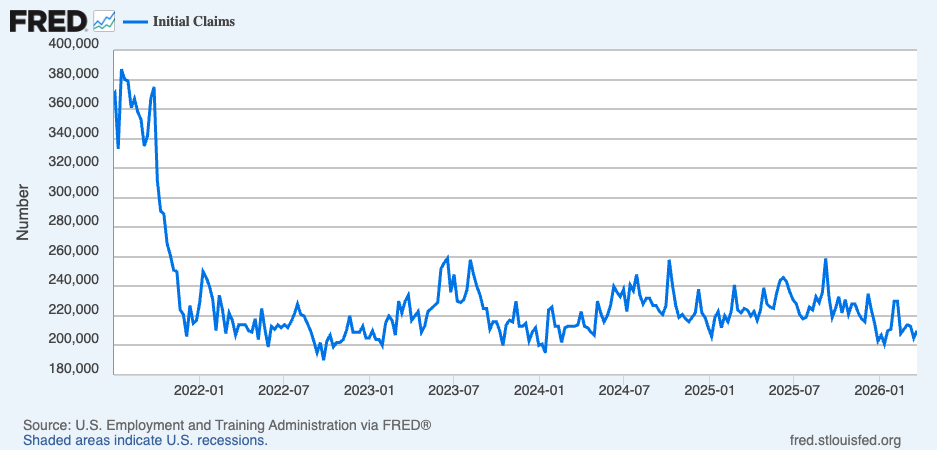

💼 New unemployment insurance claims, total ongoing claims remain low. Initial claims for unemployment benefits ticked down to 202,000 during the week ending Mar. 28, down from 211,000 the week prior. This metric remains at levels historically associated with economic growth.

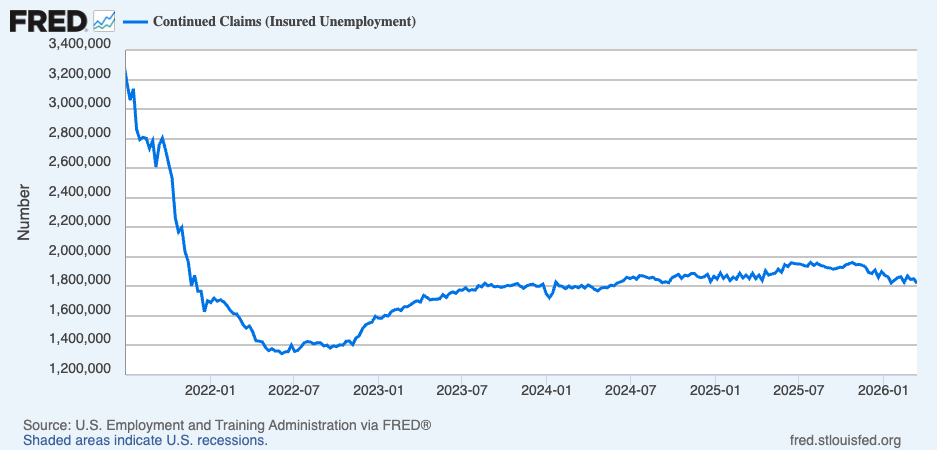

Insured unemployment, which captures those who continue to claim unemployment benefits, declined to 1.84 million during the week ending March 21.

For more on the labor market, read: The next couple of years for the job market could be tough 🫤

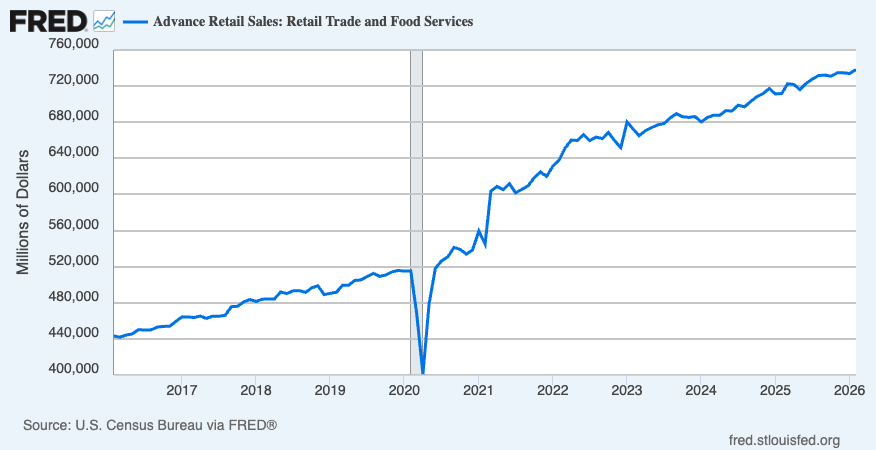

🛍️ Retail shopping activity rose. Retail sales in February increased 0.6% to a record $738.4 billion.

Most retail categories grew.

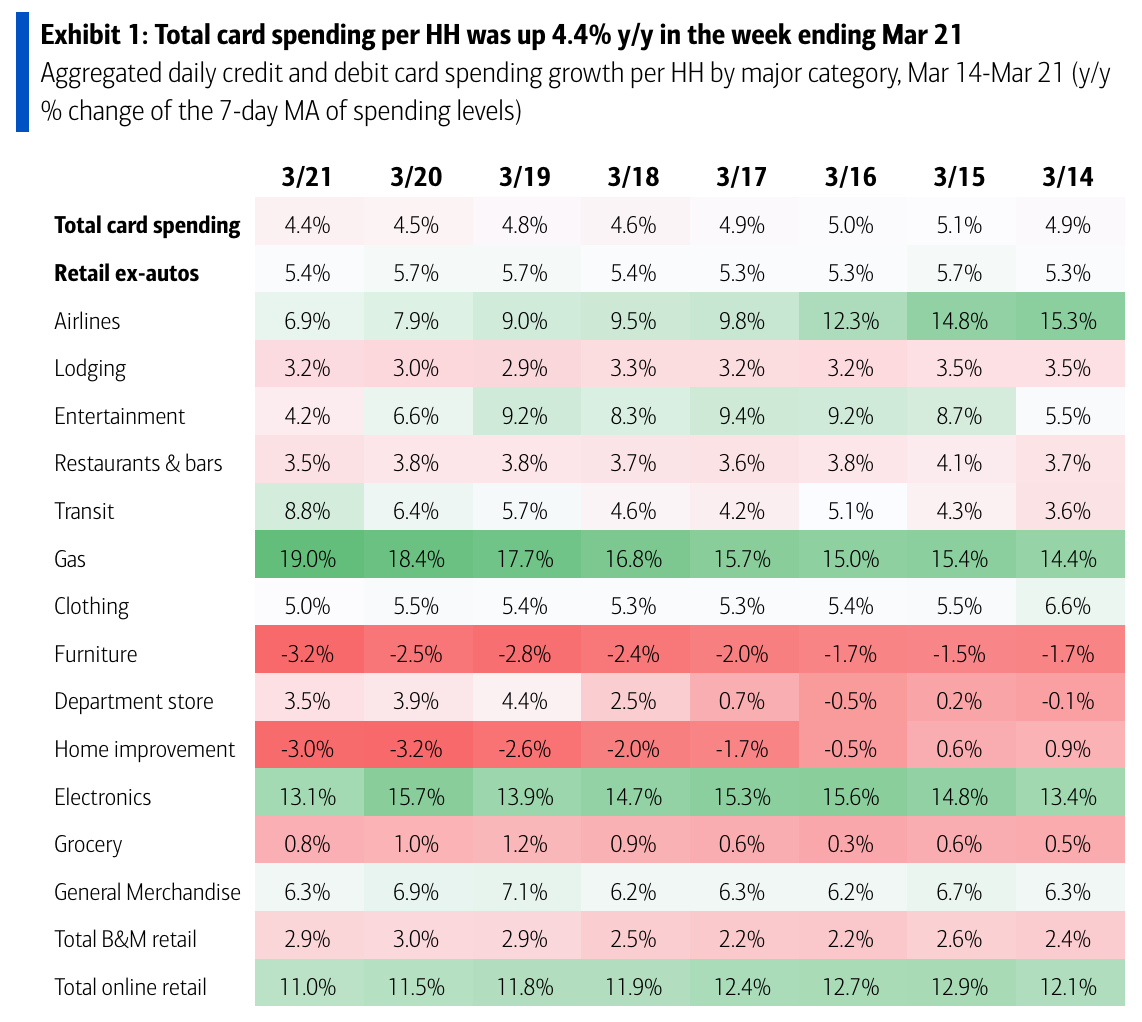

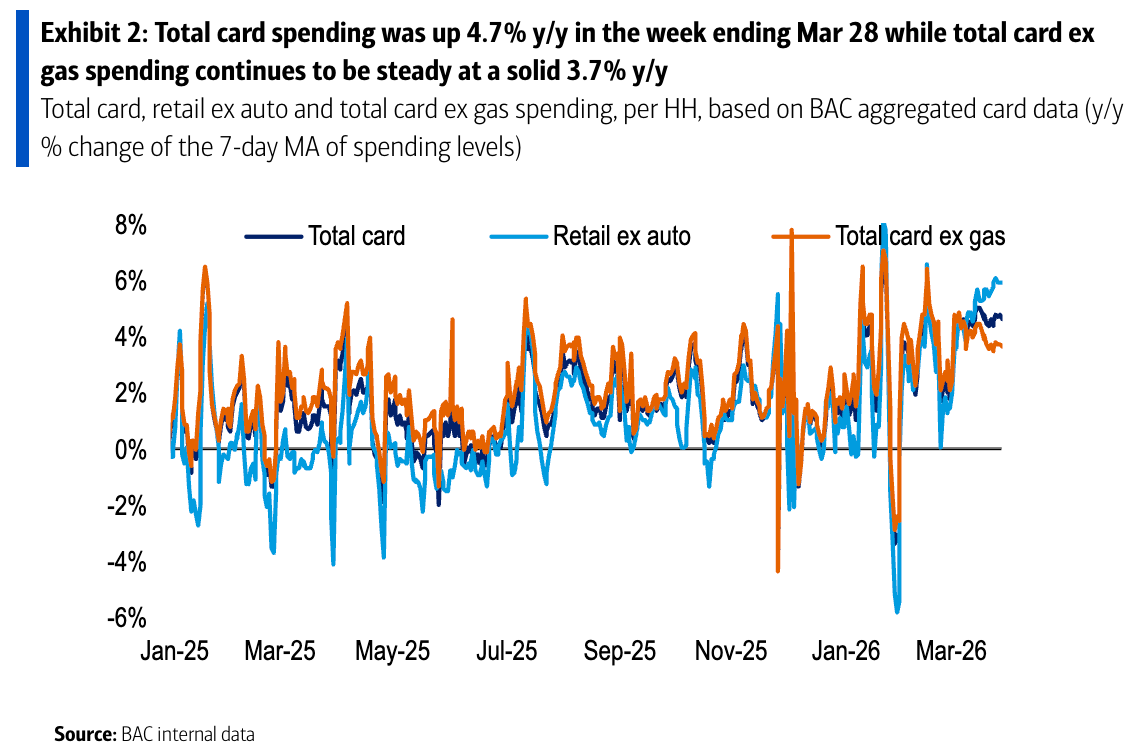

💳 Card spending data is holding up. From BofA: “Total card spending per HH was up 4.7% y/y in the week ending Mar 28, according to BAC aggregated credit & debit card data. Total card ex gas spending remains steady at a solid 3.7% y/y with a rise in home improvement & furniture since last week. Higher income HHs continue to show higher growth than other income cohorts in total ex gas spending as of week ending Mar 28.“

Consumer spending data has looked a lot better than consumer sentiment readings. For more on this contradiction, read: We’re taking that vacation whether we like it or not 🛫 and Household finances are both ‘worse’ and ‘good’ 🌦️

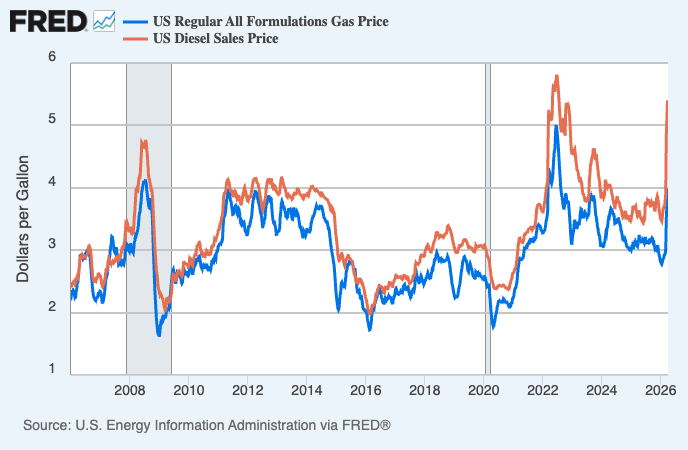

⛽️ Gas and diesel prices surge. From AAA: “The national average for a gallon of regular exceeded $4/gallon this week for the first time since August 2022. Today’s average of $4.08 is ten cents higher than last week and $1.08 higher than a month ago. Crude oil prices have been surging, surpassing $100/barrel, as the conflict in the Middle East continues and the Strait of Hormuz remains closed. In 2022, gas prices remained elevated from March through August, peaking in June when the national average reached a record of $5/gallon for one week.”

Here’s a look at the trajectory of gas and diesel prices, as tracked by the EIA.

For more on energy prices, read: Our love-hate relationship with rising oil prices in charts 💔🛢️📊

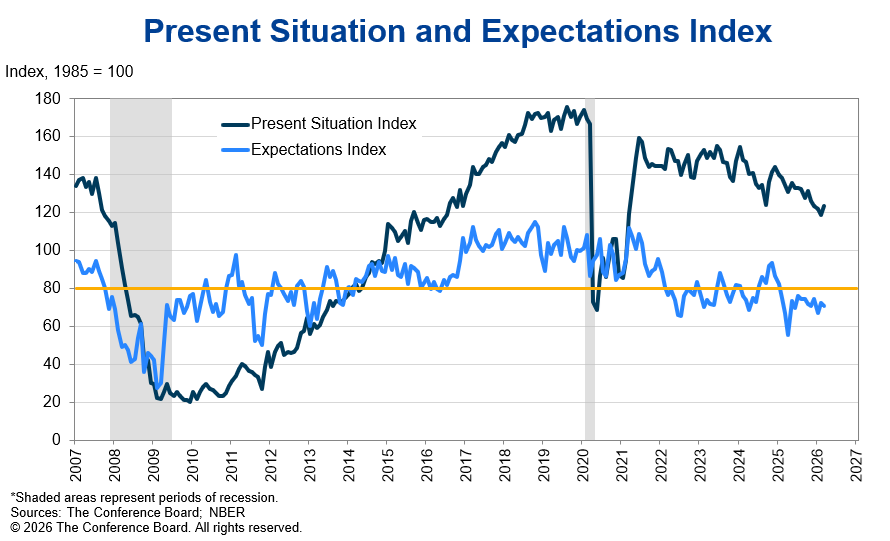

👎 Consumer vibes improve slightly, but remain in the dumps. The Conference Board’s Consumer Confidence Index climbed 0.8 points in March. From the report: “Consumer confidence ticked up again in March, as a modest improvement in consumers’ views of current conditions outweighed a slight downshift in expectations for the future. … Nonetheless, the Index has been on a general downward trend since 2021.”

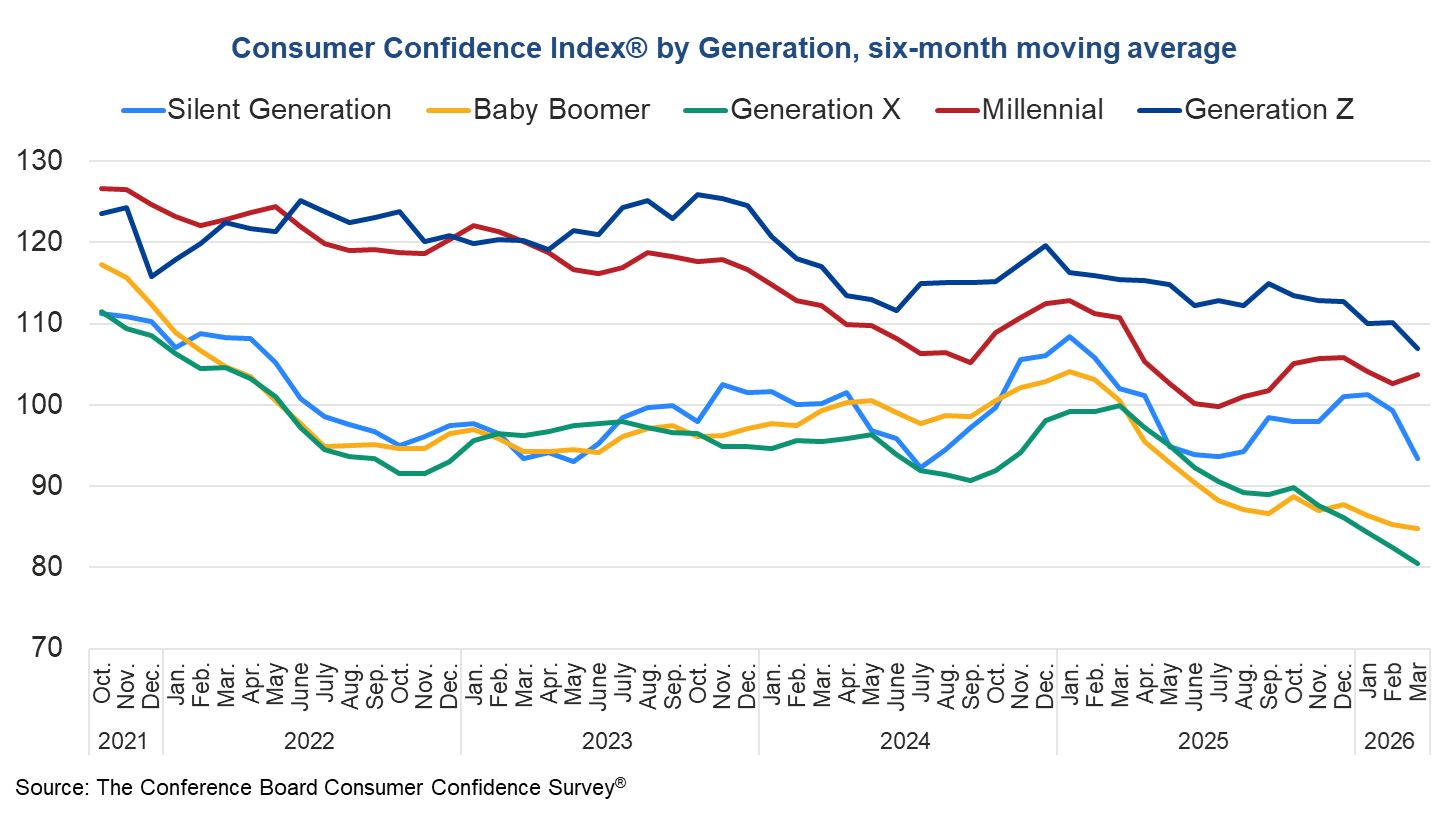

More from the report: “Among demographic groups, confidence on a six-month moving average basis continued to moderate in March for consumers under age 35 and 55 and over, and virtually unchanged after a multi-month decline for those aged 35 to 54. Respondents under 35 remain the most optimistic and those 55 and over the least. On a six-month moving average basis, Generation Z remained the most confident among all generations, but their optimism slipped in March along with the Silent Generation, Baby Boomers, and Generation X.”

For more on consumer sentiment, read: What consumers do > what consumers say 🙊 and The economy may not be working for everyone right now, but it’s at least working for stock market investors 🎭

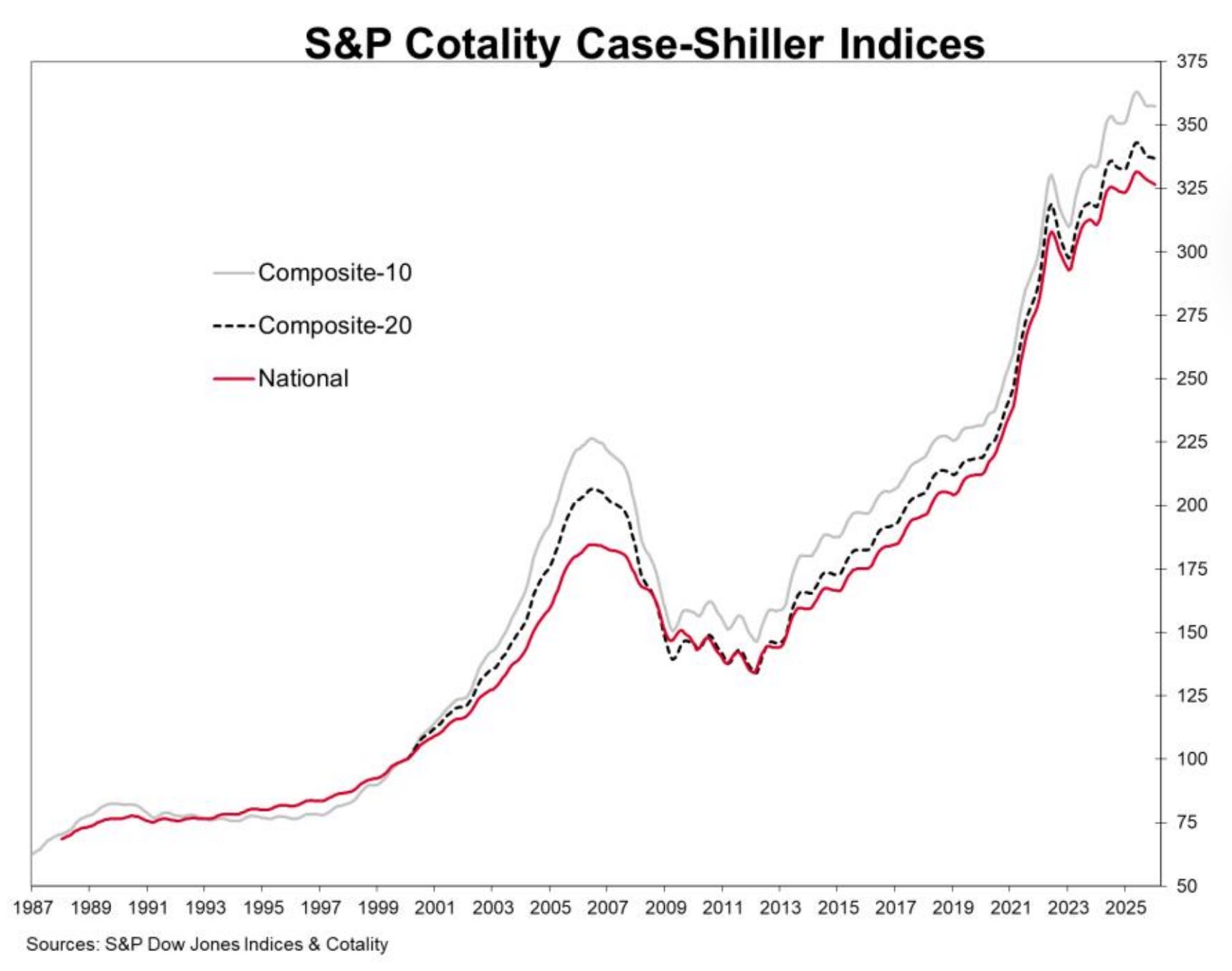

🏠 Home prices grew. According to the S&P CoreLogic Case-Shiller index, home prices were up 0.9% year-over-year in January and climbed 0.2% month-over-month. From S&P Dow Jones Indices’ Nicholas Godec: “Price levels remain elevated, but the rate of appreciation has slowed materially. Splitting the year into two halves sharpens the picture. The National Index rose 2.2% over the first six months of the period, then fell 1.3% over the most recent six — a swing that explains why annual gains have compressed to under 1% despite prices remaining historically elevated.”

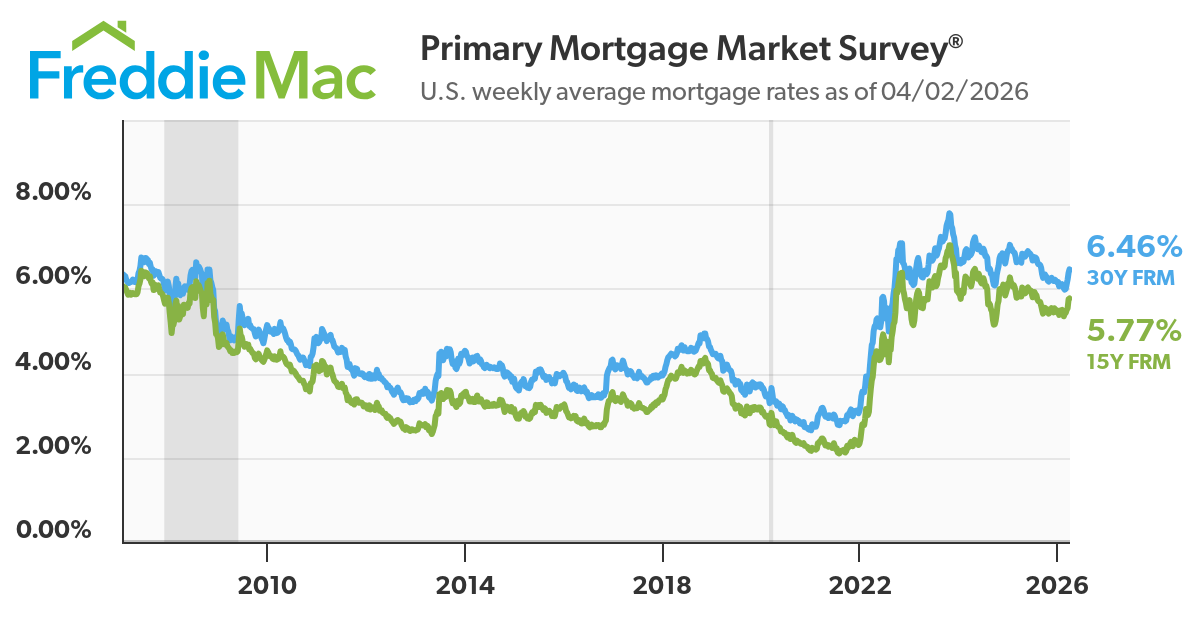

🏠 Mortgage rates rise. According to Freddie Mac, the average 30-year fixed-rate mortgage rose to 6.46%, up from 6.38% last week.

As of Q4, there were 148.7 million housing units in the U.S., of which 87.8 million were owner-occupied and about 40% were mortgage-free. Of those carrying mortgage debt, almost all have fixed-rate mortgages, and most of those mortgages have rates that were locked in before rates surged from 2021 lows. All of this is to say: Most homeowners are not particularly sensitive to the small weekly movements in home prices or mortgage rates.

For more on mortgages and home prices, read: Why home prices and rents are creating all sorts of confusion about inflation 😖

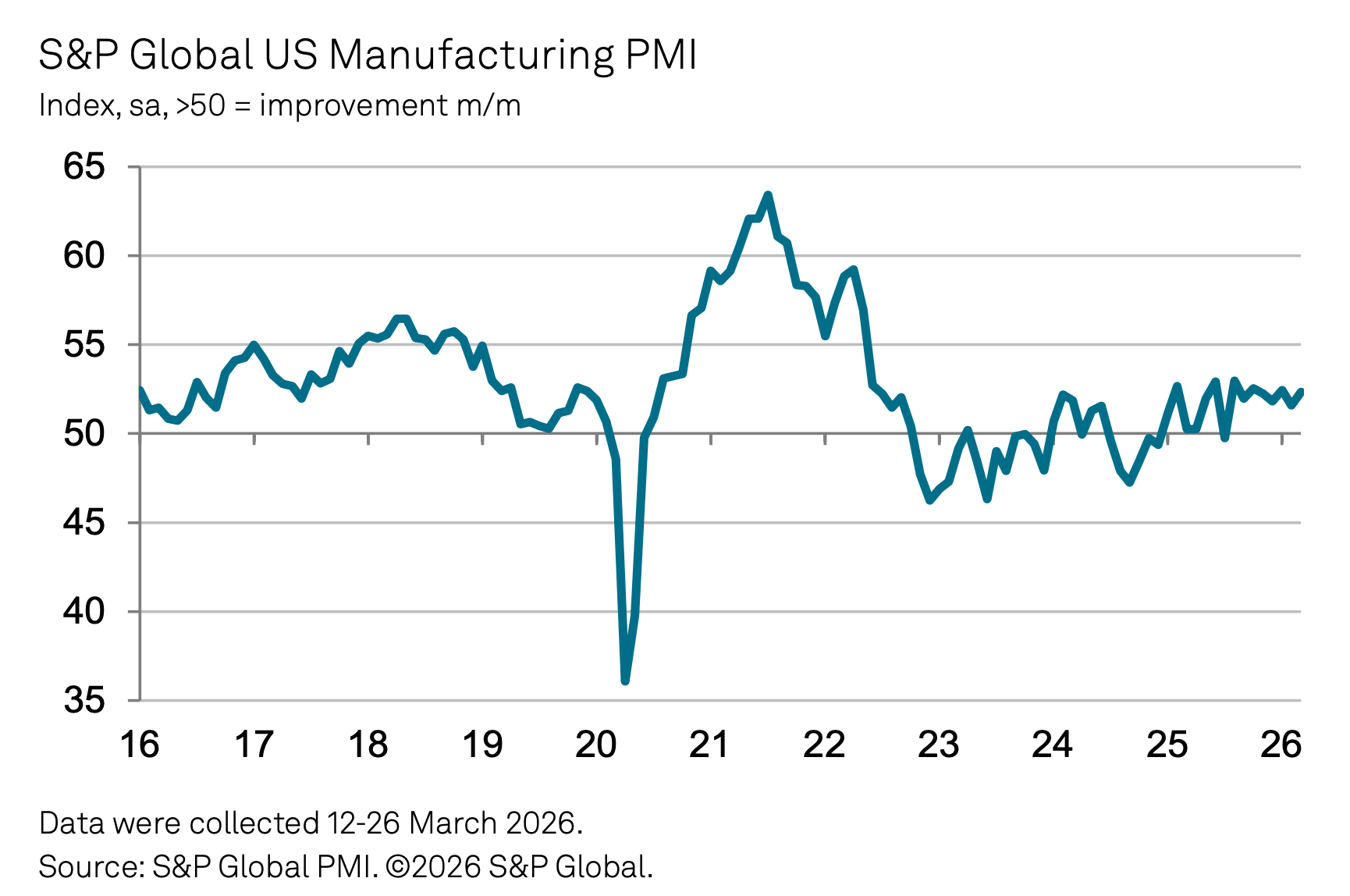

🤷 Manufacturing activity surveys signal growth, but also caution. From S&P Global’s March U.S. Manufacturing PMI: “Faster growth of output in March points to encouraging resilience for US manufacturing in the face of the outbreak of war in the Middle East. Business confidence regarding output in the year ahead has also so far held up well. This sustained resilience in part reflects reduced concerns over government policies such as tariffs, but also indicates that producers anticipate only a short-term and modest impact from the war, which is clearly uncertain. It remains early days in terms of the impact of the conflict, and a sharp rise in prices and delivery delays has cast a cloud over the outlook, threatening to drive inflation higher, dampen demand and throttle supply chains. Factory input costs have already jumped higher on the back of surging oil prices and supplier delays have become more widespread than at any time since October 2022, linked to the war exacerbating existing shipping, haulage and port delays.”

Similarly, the ISM March Manufacturing survey also signaled growth. “This month also marks the first report with panelists citing the Iran war as a new impact to their business, along with ongoing uncertainty with U.S. economic policy, despite the recent Supreme Court ruling striking down International Emergency Economic Powers Act (IEEPA) tariffs. In March, 64% of comments overall were negative. Among the negative comments, about 20% cited tariffs and about 40 percent the war in the Middle East.“

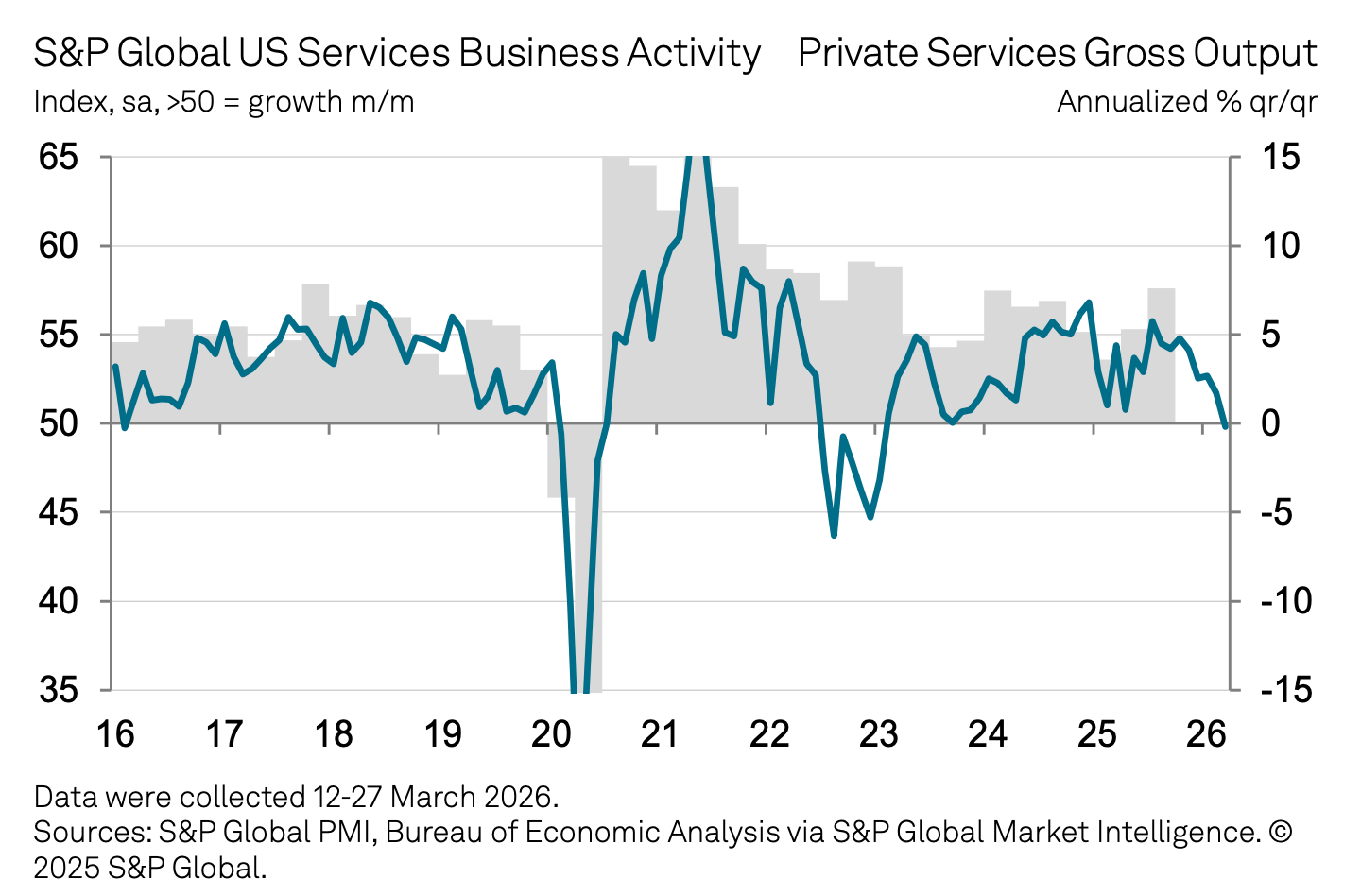

👎 Services activity survey signals contraction. From S&P Global’s March U.S. Services PMI: “The service sector has slipped into contraction for the first time since January 2023, dragging the overall economy down to a near-stalled 0.5% annualized rate of growth in March. Worst hit is consumer-facing service sectors where, barring the pandemic lockdowns, the downturn reported in March was among the steepest recorded since data were first available in 2009. However, financial services and tech, both of which performed strongly last year, have shown some signs of weaker performance amid financial market volatility and concerns over higher interest rates, which have deterred investment. Key to the deteriorating growth trend is a pull-back in spending amid worsening affordability, with costs and selling prices surging higher in March amid spiking energy prices.”

Keep in mind that during times of perceived stress, soft survey data tends to be more exaggerated than actual hard data.

For more on this, read: What businesses do > what businesses say 🙊

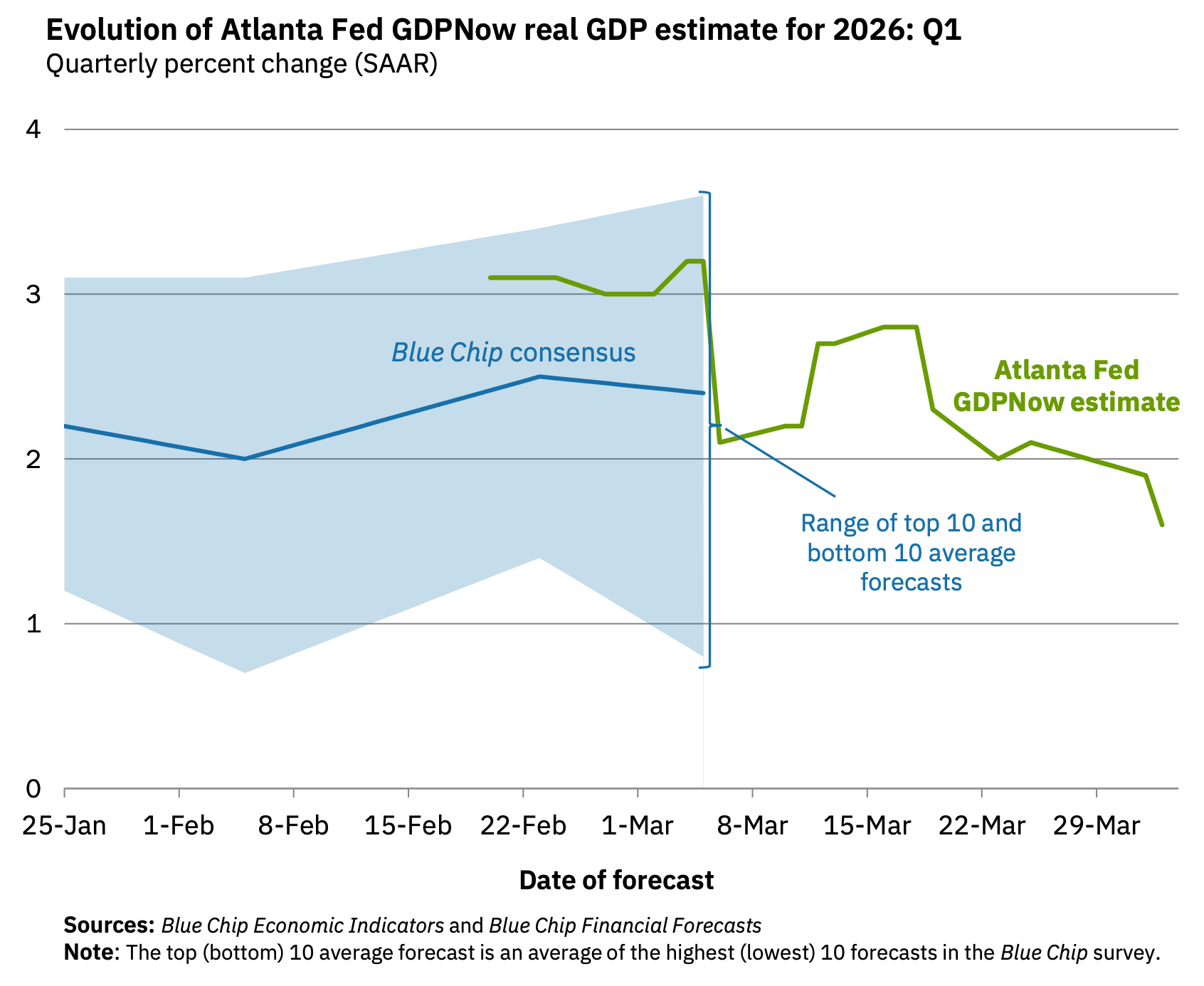

📈 Near-term GDP growth estimates are tracking positively. The Atlanta Fed’s GDPNow model sees real GDP growth rising at a 1.6% rate in Q1.

For more on GDP and the economy, read: It’s too ambiguous to just say ‘the economy’ 🤦🏻♂️ and Economic data can often be both ‘worse’ and ‘good’ 🌦️

Putting it all together 📋

Earnings look bullish: The long-term outlook for the stock market remains favorable, bolstered by expectations for years of earnings growth. And earnings are the most important driver of stock prices.

Demand is positive: Demand for goods and services remains positive, supported by healthy consumer and business balance sheets. Personal spending activity remains at record levels. Core capex orders, which are a leading indicator of business spending, have been on the rise.

Growth is cooling: While the economy remains healthy, growth has normalized from much hotter levels earlier in the cycle. The economy is less “coiled” these days as major tailwinds like job openings and excess savings have faded. Job creation is hovering at near-zero. It has become harder to argue that growth is destiny.

Actions speak louder than words: We are in an odd period, given that the hard economic data decoupled from the soft sentiment-oriented data. Consumer and business sentiment has been relatively poor, even as tangible consumer and business activity continues to grow and trend at record levels. From an investor’s perspective, what matters is that the hard economic data continues to hold up.

Stocks are not the economy: There’s a case to be made that the U.S. stock market could outperform the U.S. economy in the near term, thanks largely to positive operating leverage. Since the pandemic, companies have aggressively adjusted their cost structures. This came with strategic layoffs and investment in new equipment, including hardware powered by AI. These moves are resulting in positive operating leverage, which means a modest amount of sales growth — in the cooling economy — is translating to robust earnings growth.

Mind the ever-present risks: Of course, we should not get complacent. There will always be risks to worry about, such as U.S. political uncertainty, geopolitical turmoil, energy price volatility, and cyber attacks. There are also the dreaded unknowns. Any of these risks can flare up and spark short-term volatility in the markets.

Investing is never a smooth ride: There’s also the harsh reality that economic recessions and bear markets are developments that all long-term investors should expect as they build wealth in the markets. Always keep your stock market seat belts fastened.

Think long-term: For now, there’s no reason to believe there’ll be a challenge that the economy and the markets won’t overcome. The long game remains undefeated, and it’s a streak that long-term investors can expect to continue.

For more on how the macro story is evolving, check out the previous review of the macro crosscurrents. »

Key insights about the stock market 📈

Here’s a roundup of some of TKer’s most talked-about paid and free newsletters about the stock market. All of the headlines are hyperlinked to the archived pieces.

10 truths about the stock market 📈

The stock market can be an intimidating place: It’s real money on the line, there’s an overwhelming amount of information, and people have lost fortunes in it very quickly. But it’s also a place where thoughtful investors have long accumulated a lot of wealth. The primary difference between those two outlooks is related to misconceptions about the stock market that can lead people to make poor investment decisions.

The makeup of the S&P 500 is constantly changing 🔀

Passive investing is a concept usually associated with buying and holding a fund that tracks an index. And no passive investment strategy has attracted as much attention as buying an S&P 500 index fund. However, the S&P 500 — an index of 500 of the largest U.S. companies — is anything but a static set of 500 stocks.

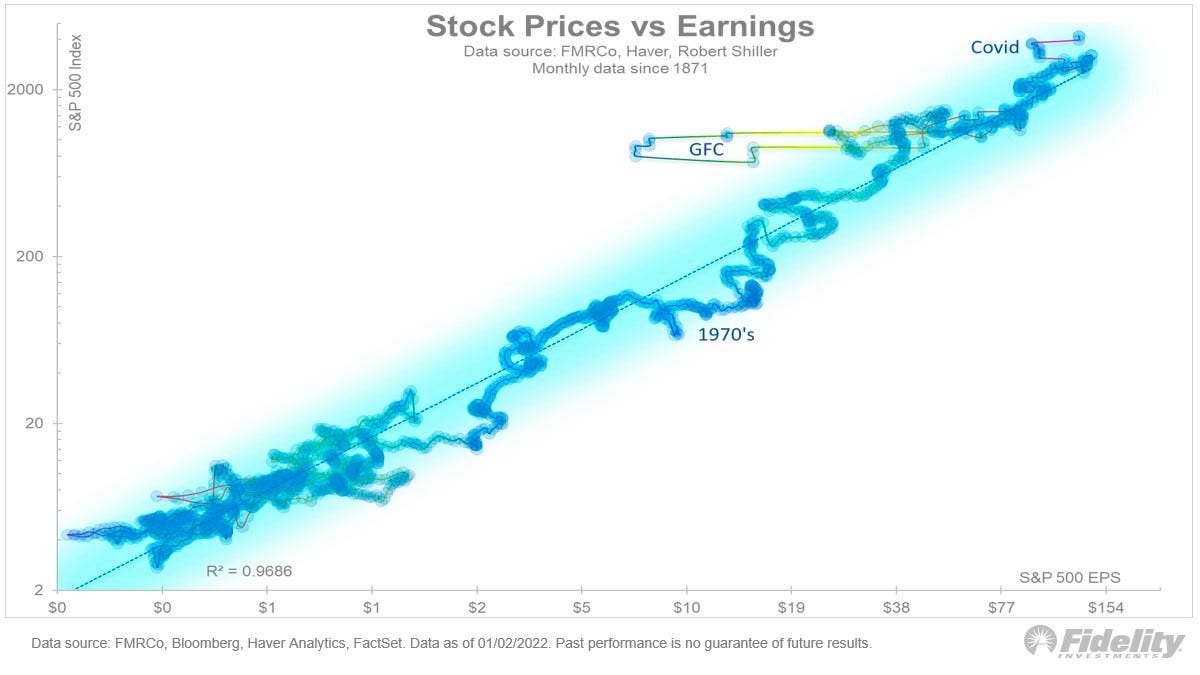

The key driver of stock prices: Earnings💰

For investors, anything you can ever learn about a company matters only if it also tells you something about earnings. That’s because long-term moves in a stock can ultimately be explained by the underlying company’s earnings, expectations for earnings, and uncertainty about those expectations for earnings. Over time, the relationship between stock prices and earnings has a very tight statistical relationship.

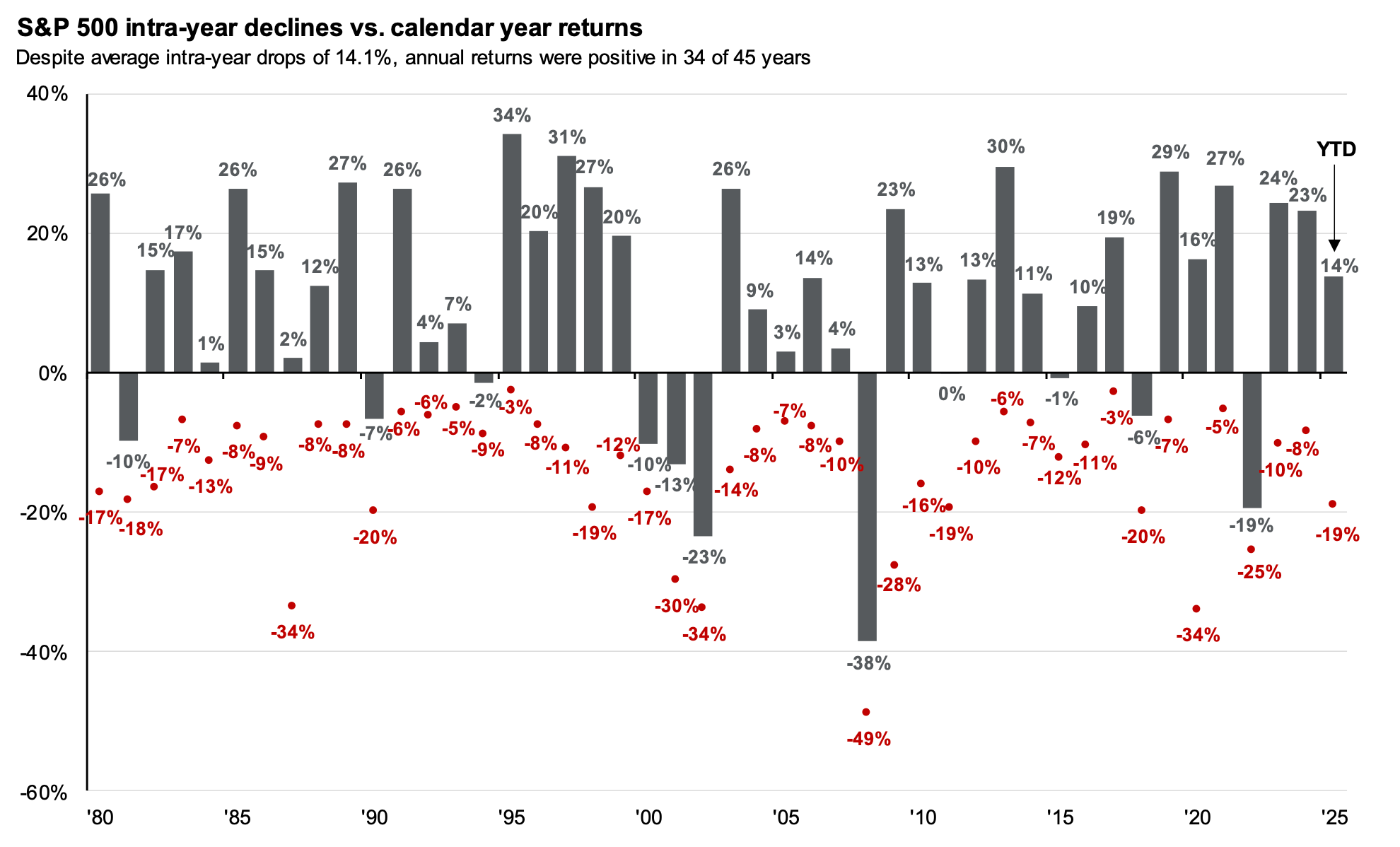

Stomach-churning stock market sell-offs are normal🎢

Investors should always be mentally prepared for some big sell-offs in the stock market. It’s part of the deal when you invest in an asset class that is sensitive to the constant flow of good and bad news. Since 1950, the S&P 500 has seen an average annual max drawdown (i.e., the biggest intra-year sell-off) of 14%.

How the stock market performed around recessions 📉📈

Every recession in history was different. And the range of stock performance around them varied greatly. There are two things worth noting. First, recessions have always been accompanied by a significant drawdown in stock prices. Second, the stock market bottomed and inflected upward long before recessions ended.

In the stock market, time pays ⏳

Since 1928, the S&P 500 has generated a positive total return more than 89% of the time over all five-year periods. Those are pretty good odds. When you extend the timeframe to 20 years, you’ll see that there’s never been a period where the S&P 500 didn’t generate a positive return.

What a strong dollar means for stocks 👑

While a strong dollar may be great news for Americans vacationing abroad and U.S. businesses importing goods from overseas, it’s a headwind for multinational U.S.-based corporations doing business in non-U.S. markets.

Stanley Druckenmiller's No. 1 piece of advice for novice investors 🧐

…you don't want to buy them when earnings are great, because what are they doing when their earnings are great? They go out and expand capacity. Three or four years later, there's overcapacity and they're losing money. What about when they're losing money? Well, then they’ve stopped building capacity. So three or four years later, capacity will have shrunk and their profit margins will be way up. So, you always have to sort of imagine the world the way it's going to be in 18 to 24 months as opposed to now. If you buy it now, you're buying into every single fad every single moment. Whereas if you envision the future, you're trying to imagine how that might be reflected differently in security prices.

Peter Lynch made a remarkably prescient market observation in 1994 🎯

Some event will come out of left field, and the market will go down, or the market will go up. Volatility will occur. Markets will continue to have these ups and downs. … Basic corporate profits have grown about 8% a year historically. So, corporate profits double about every nine years. The stock market ought to double about every nine years… The next 500 points, the next 600 points — I don’t know which way they’ll go… They’ll double again in eight or nine years after that. Because profits go up 8% a year, and stocks will follow. That's all there is to it.

Warren Buffett's 'fourth law of motion' 📉

Long ago, Sir Isaac Newton gave us three laws of motion, which were the work of genius. But Sir Isaac’s talents didn’t extend to investing: He lost a bundle in the South Sea Bubble, explaining later, “I can calculate the movement of the stars, but not the madness of men.” If he had not been traumatized by this loss, Sir Isaac might well have gone on to discover the Fourth Law of Motion: For investors as a whole, returns decrease as motion increases.

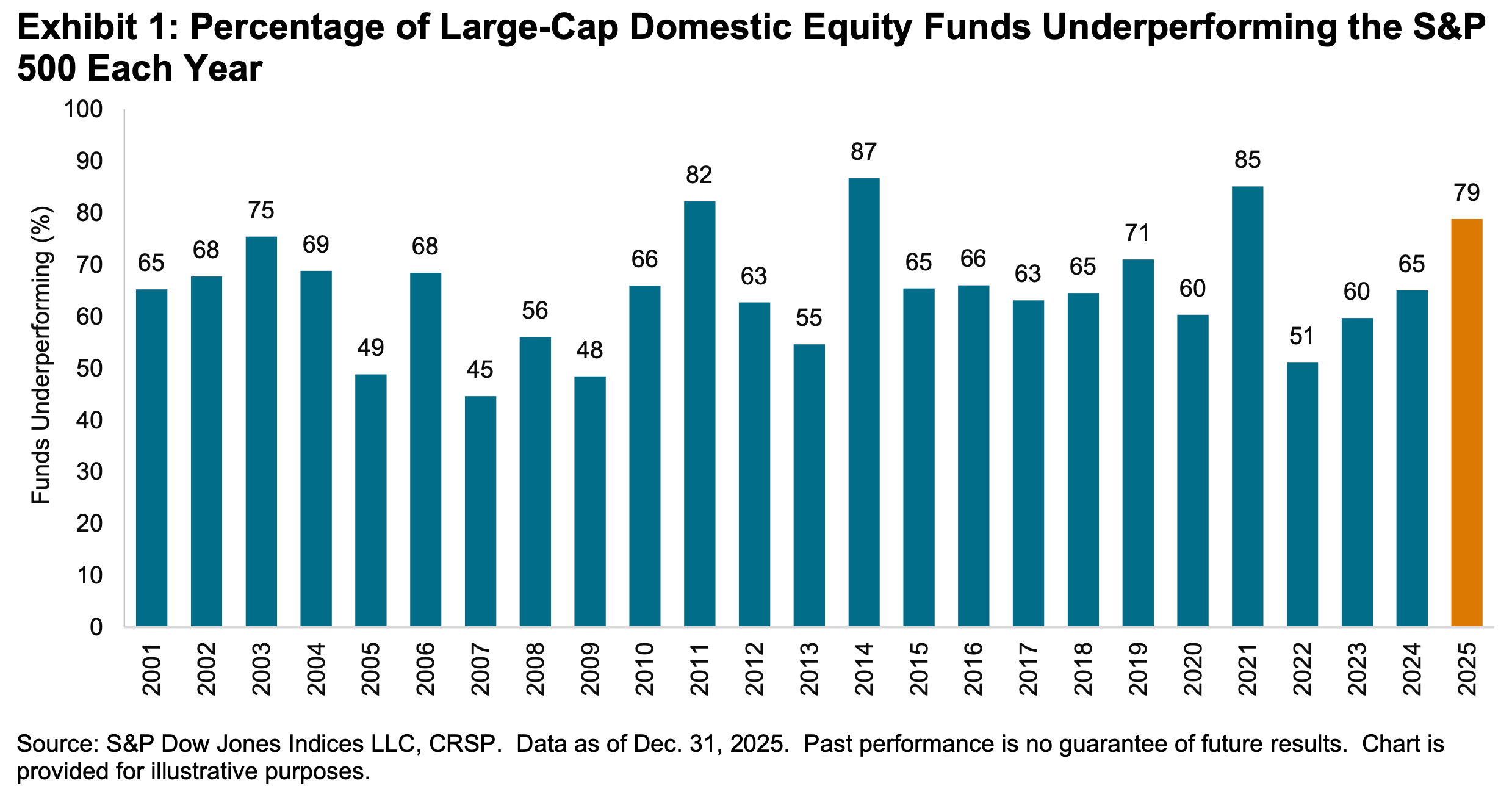

Most pros can’t beat the market 🥊

According to S&P Dow Jones Indices (SPDJI), 79% of U.S. large-cap equity fund managers underperformed the S&P 500 in 2025. As you stretch the time horizon, the numbers get even more dismal. Over three years, 67% underperformed. Over 5 years, 89% underperformed. And over 20 years, 93% underperformed. This 2025 performance was the 16th consecutive year in which the majority of fund managers in this category have lagged the index.

Proof that 'past performance is no guarantee of future results' 📊

Even if you are a fund manager who generated industry-leading returns in one year, history says it’s an almost insurmountable task to stay on top consistently in subsequent years. According to S&P Dow Jones Indices, just 4.21% of all U.S. equity funds in the top half of performance during the first year were able to remain in the top during the four subsequent years. Only 2.42% of U.S. large-cap funds remained in the top half

SPDJI’s report also considered fund performance relative to their benchmarks over the past three years. Of 738 U.S. large-cap equity funds tracked by SPDJI, 50.68% beat the S&P 500 in 2022. Just 5.08% beat the S&P in the two years ending 2023. And only 2.14% of the funds beat the index over the three years ending in 2024.

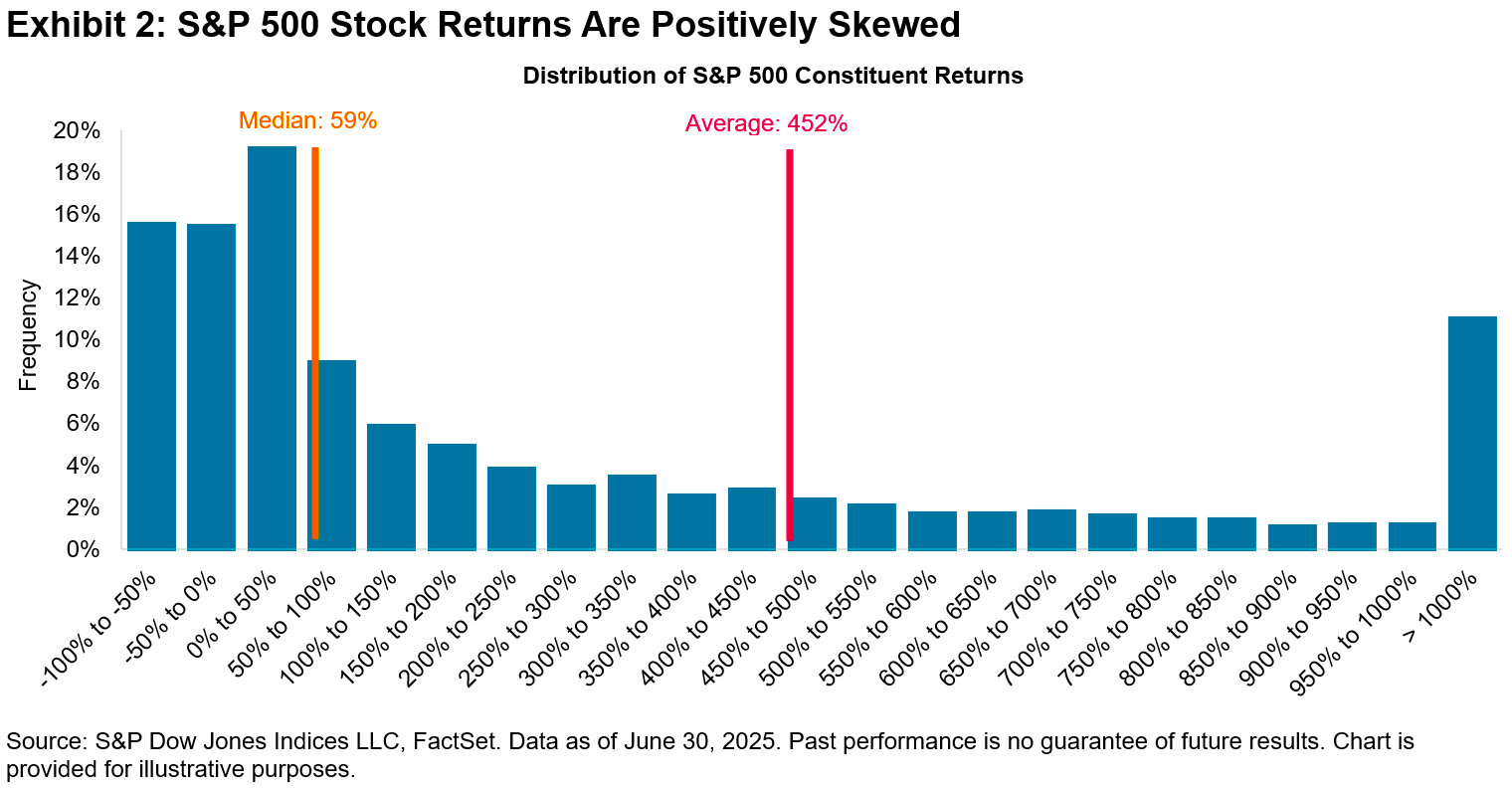

The odds are stacked against stock pickers 🎲

Picking stocks in an attempt to beat market averages is an incredibly challenging and sometimes money-losing effort. Most professional stock pickers aren’t able to do this consistently. One of the reasons for this is that most stocks don’t deliver above-average returns. According to S&P Dow Jones Indices, only 19% of the stocks in the S&P 500 outperformed the average stock’s return from 2001 to 2025. Over this period, the average return on an S&P 500 stock was 452%, while the median stock rose by just 59%.